Mastering the 2026 Roth IRA Conversion: A 15% Tax Savings Blueprint

In the ever-evolving landscape of retirement planning, proactive strategies are not just beneficial; they are essential for maximizing your financial future. As we look towards 2026, a significant opportunity emerges for many savvy investors: the Roth IRA 2026 Conversion. This strategy could potentially allow you to lock in substantial tax savings, possibly upwards of 15% or more, on your retirement income. But what exactly is a Roth IRA conversion, why is 2026 a pivotal year, and how can you leverage this opportunity to your advantage? This comprehensive guide will delve into the intricacies of the 2026 Roth IRA conversion, providing you with the knowledge and tools to make informed decisions for your retirement nest egg.

Retirement planning often feels like navigating a complex maze, with tax codes, investment choices, and future uncertainties at every turn. However, understanding and strategically utilizing vehicles like the Roth IRA can simplify this journey dramatically. The allure of tax-free withdrawals in retirement is a powerful motivator, and for many, a Roth conversion can be the key to achieving this coveted financial freedom. The year 2026 isn’t just another date on the calendar; it represents a specific window of opportunity tied to potential changes in tax legislation, making it a crucial focal point for those considering a Roth conversion.

Understanding the Roth IRA and Its Advantages

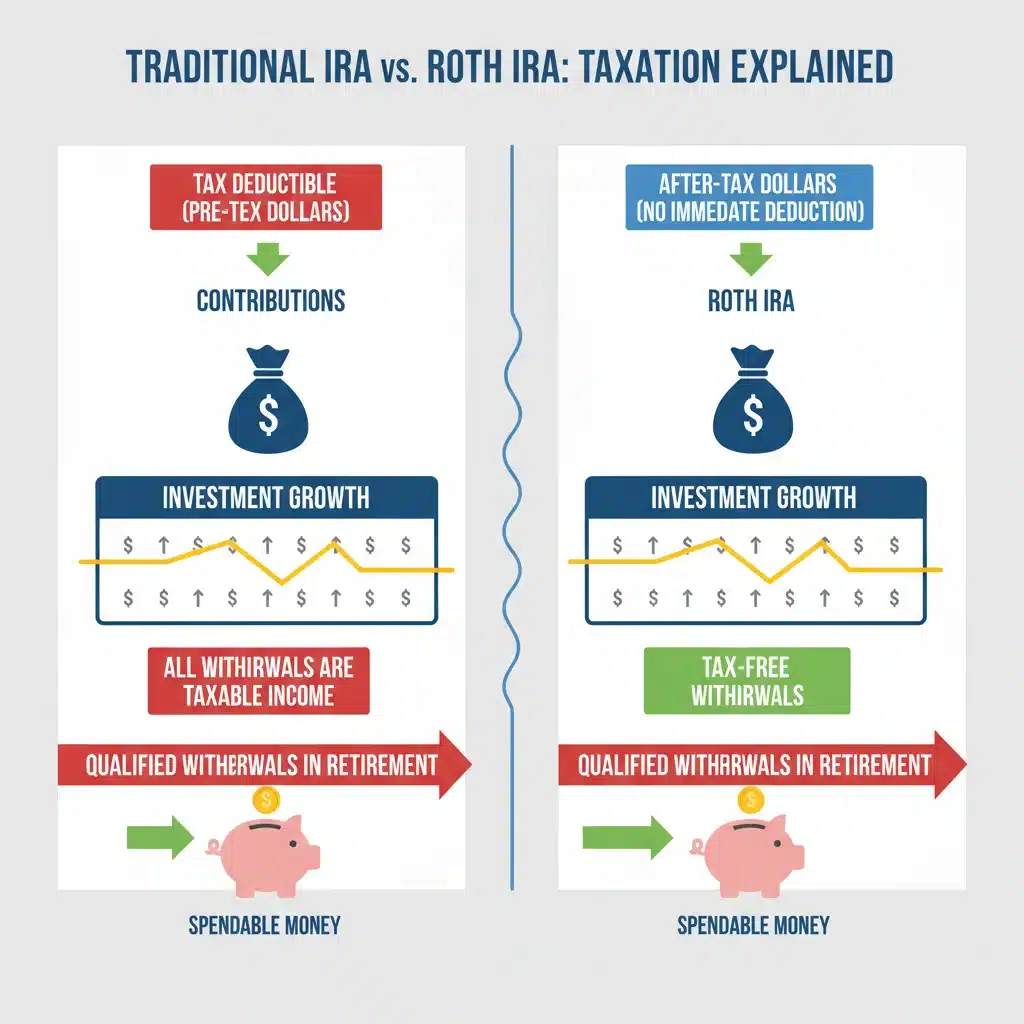

Before we dive into the specifics of the Roth IRA 2026 Conversion, let’s establish a foundational understanding of what a Roth IRA is and why it’s such a powerful retirement tool. Unlike traditional IRAs, where contributions are often tax-deductible and withdrawals in retirement are taxed, Roth IRAs operate on a different principle: you contribute after-tax dollars, and in return, qualified withdrawals in retirement are completely tax-free. This fundamental difference is what makes Roth IRAs incredibly appealing, especially for those who anticipate being in a higher tax bracket during retirement than they are today.

The primary advantage of a Roth IRA lies in its tax-free growth and withdrawals. Imagine your investments growing for decades, compounding year after year, and then being able to access all that growth without owing a single penny in federal income tax. This is the promise of the Roth IRA. Furthermore, Roth IRAs do not have required minimum distributions (RMDs) for the original owner during their lifetime, offering greater flexibility in managing your retirement income and estate planning. This can be particularly beneficial for those who plan to work longer or have other income sources in retirement and prefer to leave their Roth IRA assets to grow for a longer period or pass them on to heirs.

Another often-overlooked benefit is the ability to withdraw contributions tax-free and penalty-free at any time, for any reason. While it’s generally advisable to keep retirement funds invested, this liquidity can serve as an emergency fund if absolutely necessary, adding a layer of financial security. For these reasons and more, the Roth IRA stands out as a cornerstone of a well-rounded retirement strategy.

What is a Roth IRA Conversion?

A Roth IRA conversion, sometimes referred to as a "backdoor Roth" if specific income limits apply, is the process of moving funds from a traditional IRA, 401(k), or other pre-tax retirement account into a Roth IRA. When you convert, the amount converted from the pre-tax account becomes taxable income in the year of the conversion. This is the crucial point: you pay the taxes now, at your current marginal tax rate, in exchange for tax-free withdrawals in retirement.

The decision to convert hinges on several factors, most notably your current tax bracket versus your anticipated future tax bracket. If you believe your tax rate will be higher in retirement than it is today, a Roth conversion can be a highly effective tax-saving maneuver. By paying taxes now at a lower rate, you avoid paying them later at a potentially higher rate, effectively locking in your tax liability. This foresight is what makes the Roth IRA 2026 Conversion particularly relevant, as we’ll explore shortly.

It’s important to understand that there are no income limitations for performing a Roth conversion. While there are income limits for directly contributing to a Roth IRA, anyone can convert funds from a traditional IRA to a Roth IRA, regardless of their income. This makes the conversion strategy accessible to high-income earners who are otherwise phased out of direct Roth contributions, often utilizing the "backdoor Roth" strategy.

Why 2026 is a Critical Year for Roth Conversions

The significance of 2026 for the Roth IRA 2026 Conversion strategy is rooted in current tax legislation. The Tax Cuts and Jobs Act (TCJA) of 2017 introduced a series of individual income tax rate reductions that are set to expire at the end of 2025. This means that, absent new legislation, tax rates for individuals are scheduled to revert to their pre-TCJA levels starting in 2026. For many taxpayers, this would mean an increase in their marginal income tax rates.

Consider the implications: if you convert a traditional IRA to a Roth IRA in 2025, you would pay taxes on that converted amount at the potentially lower TCJA rates. If you wait until 2026 or later, you might face higher tax rates on the same converted amount. This potential increase in tax rates creates a powerful incentive to consider a Roth conversion sooner rather than later, specifically before the end of 2025, to take advantage of the current, more favorable tax environment.

For example, if your current marginal tax rate is 24% and it’s projected to increase to 28% or even 33% in 2026, converting now could save you that 4% to 9% difference on the converted amount. Over a large sum, this can translate into substantial savings, easily reaching the 15% or more mentioned in our title when factoring in the long-term tax-free growth. The window of opportunity to capitalize on these potentially lower tax rates is narrowing, making strategic planning for a Roth IRA 2026 Conversion a timely discussion.

Calculating the Potential 15% Tax Savings

Let’s illustrate how a 15% or greater tax savings could materialize with a Roth IRA 2026 Conversion. This isn’t a guaranteed figure, as individual circumstances vary, but it highlights the potential impact. Suppose you have $100,000 in a traditional IRA. If you convert this in 2025 while your marginal tax rate is, for instance, 22%, you would pay $22,000 in taxes on the conversion.

Now, let’s project forward. If you were to leave that $100,000 in the traditional IRA and withdraw it in retirement when your marginal tax rate is, say, 37% (a plausible scenario if tax rates revert or if you have significant retirement income), you would pay $37,000 in taxes. The immediate savings on the conversion itself would be $15,000 ($37,000 – $22,000), which is exactly 15% of the original $100,000 converted amount.

But the savings don’t stop there. The $100,000 in the Roth IRA will continue to grow tax-free. If that $100,000 grows to $200,000 over 10-15 years, and you withdraw it tax-free, you’ve avoided taxes on an additional $100,000 of growth. If your retirement tax rate is 37%, that’s another $37,000 in saved taxes on the growth alone. Combining the immediate savings on the conversion with the long-term tax-free growth, the total tax savings can far exceed 15%, making the Roth IRA 2026 Conversion a compelling strategy.

Key Considerations Before Converting

While the prospect of tax savings is enticing, a Roth IRA conversion is not a one-size-fits-all solution. Several factors warrant careful consideration before you proceed with a Roth IRA 2026 Conversion:

- Your Current and Future Tax Brackets: This is arguably the most critical factor. If you expect to be in a significantly lower tax bracket in retirement, a Roth conversion might not be advantageous, as you’d be paying taxes now at a higher rate. Conversely, if you anticipate higher future tax rates, converting now makes more sense.

- Taxable Income in the Year of Conversion: Remember, the converted amount is added to your taxable income for the year. A large conversion could push you into a higher tax bracket, diminishing the benefits. Strategic planning, potentially spreading conversions over several years (a "laddering" strategy), can help manage this.

- Ability to Pay the Taxes: You must have funds available to pay the taxes due on the conversion, ideally from outside your retirement accounts. Paying the taxes from the converted amount itself reduces the amount that gets to grow tax-free in the Roth IRA, which is generally not recommended.

- Time Horizon: The longer your money has to grow tax-free in the Roth IRA, the greater the benefit. If retirement is many years away, the compounding effect of tax-free growth becomes incredibly powerful.

- Required Minimum Distributions (RMDs): If you are approaching RMD age (currently 73), converting traditional IRA funds to a Roth IRA can eliminate future RMDs on those converted assets, offering greater control over your retirement income.

- Medicare Premiums (IRMAA): A large Roth conversion in a single year could increase your Adjusted Gross Income (AGI), potentially leading to higher Medicare Part B and Part D premiums two years down the line (Income-Related Monthly Adjustment Amount, or IRMAA). This is another reason to consider spreading conversions over multiple years.

- State Taxes: Don’t forget state income taxes. Some states tax Roth conversions, while others do not. Factor this into your overall tax calculation.

Each of these points needs careful evaluation in the context of your unique financial situation. Consulting with a qualified financial advisor or tax professional is highly recommended to assess the optimal strategy for your Roth IRA 2026 Conversion.

Strategies for an Optimal Roth IRA 2026 Conversion

To truly maximize the benefits of a Roth IRA 2026 Conversion, consider these advanced strategies:

1. The "Laddering" Strategy

Instead of converting a large sum all at once, consider converting smaller amounts over several years. This "laddering" approach can help you manage your taxable income each year, preventing you from being bumped into a higher tax bracket by a single large conversion. It also allows you to take advantage of any dips in your income or changes in tax legislation. For example, you might convert a portion in 2024, another in 2025, and then reassess for 2026 based on the new tax landscape.

2. Utilizing Low-Income Years

If you anticipate a year with lower-than-usual income (e.g., due to a job change, sabbatical, or early retirement), this can be an opportune time to perform a Roth conversion. With less other income, the converted amount will be taxed at a lower marginal rate, maximizing your savings. This is a prime example of strategic timing for your Roth IRA 2026 Conversion.

3. Converting After a Market Downturn

Converting traditional IRA assets after a market downturn can be a highly effective strategy. When your IRA balance is temporarily lower, you’re converting fewer dollars, meaning you pay taxes on a smaller amount. As the market recovers, the assets in your Roth IRA will grow tax-free from that lower converted base, amplifying your long-term tax savings. This requires a strong stomach and a belief in market recovery, but the rewards can be significant.

4. The Backdoor Roth IRA (for High Earners)

If your income exceeds the IRS limits for direct Roth IRA contributions, the backdoor Roth strategy allows you to effectively contribute to a Roth IRA. This involves contributing after-tax money to a traditional IRA (where there are no income limits for non-deductible contributions) and then immediately converting those funds to a Roth IRA. While the initial contribution is non-deductible, the conversion itself is largely tax-free, assuming you have no other pre-tax traditional IRA balances (which would trigger the "pro-rata" rule). This is a vital strategy for high-income individuals looking to benefit from the Roth IRA 2026 Conversion advantages.

5. Consider Tax Loss Harvesting

If you have taxable investment accounts with losses, you might be able to use tax loss harvesting to offset some of the income generated by a Roth conversion. By selling investments at a loss, you can typically deduct up to $3,000 of capital losses against ordinary income per year, and carry forward any excess losses to future years. This can help reduce the tax burden of your Roth IRA 2026 Conversion.

Potential Pitfalls and How to Avoid Them

While the benefits of a Roth IRA 2026 Conversion are substantial, there are potential pitfalls to be aware of:

- Overlooking the Pro-Rata Rule: If you have existing pre-tax traditional IRAs, the IRS’s "pro-rata" rule comes into play. This rule states that you cannot pick and choose which dollars you convert. Instead, a portion of your conversion will be considered pre-tax and taxable, even if you only convert after-tax contributions. This can make the backdoor Roth strategy more complex and potentially less tax-efficient if you have significant pre-tax IRA balances.

- Not Having Funds for Taxes: As mentioned, paying taxes on the conversion from the converted amount itself is generally a bad idea. It reduces the amount that gets to grow tax-free and can trigger early withdrawal penalties if you’re under 59½ and the funds haven’t been in the traditional IRA for at least five years.

- Misjudging Future Tax Brackets: Predicting future tax rates is challenging. A conversion is most beneficial if your tax rate is lower now than it will be in retirement. If your income drops significantly in retirement, a conversion might have been premature.

- Ignoring the Five-Year Rule: For Roth conversions, there’s a separate five-year rule for withdrawals. While contributions can be withdrawn tax-free and penalty-free at any time, converted amounts must generally remain in the Roth IRA for five years (from January 1st of the year of conversion) to be withdrawn penalty-free if you are under 59½. This rule applies to each conversion separately.

- Failing to Consult a Professional: The complexities of tax law and retirement planning necessitate professional guidance. A financial advisor or tax professional can help you navigate these rules, analyze your specific situation, and project potential outcomes, ensuring your Roth IRA 2026 Conversion is optimized.

The Role of Tax Planning in Your Roth Conversion

Effective tax planning is not merely an annual exercise; it’s a continuous process that profoundly impacts your long-term financial health, especially when considering a Roth IRA 2026 Conversion. This strategic move requires a deep understanding of current tax laws, anticipated future tax legislation, and your personal financial trajectory.

One critical aspect of tax planning for a Roth conversion involves forecasting your income and deductions for the conversion year. A large conversion could push you into a higher marginal tax bracket, increasing the tax liability on the converted amount. By strategically managing other income and deductions, or by spreading conversions over multiple years, you can mitigate this risk. For instance, if you anticipate a year with lower capital gains or fewer bonuses, that might be an ideal time to execute a portion of your Roth conversion.

Furthermore, tax planning should consider the impact on other areas of your financial life. As previously mentioned, an increase in Adjusted Gross Income (AGI) due to a Roth conversion can influence eligibility for certain tax credits, deductions, and even the cost of Medicare premiums. A holistic view, taking into account all these interconnected elements, is paramount. This is where a skilled tax professional can provide invaluable insights, helping you model various conversion scenarios and identify the most tax-efficient path forward for your Roth IRA 2026 Conversion.

Integrating Roth Conversions into Your Overall Retirement Strategy

A Roth IRA 2026 Conversion should not be viewed as an isolated transaction but rather as an integral component of your broader retirement strategy. It complements other retirement savings vehicles and investment decisions, working in concert to achieve your long-term financial goals.

For example, if you have a mix of pre-tax accounts (like traditional IRAs and 401(k)s) and taxable brokerage accounts, a Roth conversion can help diversify your tax exposure in retirement. By having funds in all three "tax buckets" (taxable, tax-deferred, and tax-free), you gain flexibility in retirement to withdraw from the account that offers the most tax-efficient outcome in any given year. This tax diversification is a powerful tool for managing your future tax bill.

Moreover, for those concerned about leaving a tax-efficient legacy, Roth IRAs are an excellent estate planning tool. Because they do not have RMDs for the original owner and qualified withdrawals are tax-free for beneficiaries (subject to certain rules), they can be a highly effective way to transfer wealth to future generations without burdening them with significant tax liabilities. Planning your Roth IRA 2026 Conversion with an eye towards estate planning can significantly enhance its value.

Finally, consider how a Roth conversion fits with your overall investment strategy. The assets within a Roth IRA can be invested in a wide range of securities, just like a traditional IRA. If you have high-growth potential investments, placing them within a Roth IRA allows all that growth to be tax-free, magnifying the benefits of the conversion. This synergy between investment selection and tax strategy is what makes the Roth IRA 2026 Conversion such a potent financial planning tool.

Conclusion: Seizing the 2026 Roth IRA Conversion Opportunity

The Roth IRA 2026 Conversion presents a unique and potentially highly lucrative opportunity for individuals looking to optimize their retirement savings and significantly reduce their future tax burden. With the scheduled expiration of the Tax Cuts and Jobs Act’s individual income tax rate reductions at the end of 2025, the window to convert at potentially lower tax rates is a critical consideration for many.

By understanding the mechanics of a Roth conversion, carefully evaluating your current and future tax situations, and employing strategic planning techniques like laddering conversions or utilizing low-income years, you can position yourself to save 15% or more on taxes that would otherwise be due in retirement. The long-term benefits of tax-free growth and withdrawals, coupled with the flexibility and estate planning advantages of a Roth IRA, make this strategy incredibly compelling.

However, the decision to convert is complex and deeply personal. It requires a thorough analysis of your financial situation, an understanding of current and projected tax laws, and a clear vision for your retirement. While this guide provides a comprehensive overview, the importance of consulting with a qualified financial advisor or tax professional cannot be overstated. They can help you navigate the intricacies, conduct personalized projections, and ensure that your Roth IRA 2026 Conversion strategy aligns perfectly with your broader financial goals and aspirations.

Don’t let this potential opportunity pass you by. Start the conversation with your financial planner today to explore how the 2026 Roth IRA conversion can be a cornerstone of your tax-efficient retirement future.

& IRA for 2025")