Estate Tax Planning 2026: Strategies to Reduce Heirs’ Tax Burden by 40%

Estate Tax Planning 2026: Essential Strategies to Reduce Your Heirs’ Tax Burden by up to 40%

As we approach 2026, the landscape of estate tax laws is poised for significant changes that could profoundly impact how you transfer wealth to your heirs. Understanding and proactively addressing these shifts through effective estate tax planning 2026 is not just a recommendation; it’s a necessity. Without proper foresight and strategic action, your beneficiaries could face a substantial reduction in their inheritance, potentially up to 40% or more, due to federal and state estate taxes. This comprehensive guide delves into the crucial strategies you need to implement now to safeguard your legacy and ensure your loved ones receive the maximum benefit from your lifetime of hard work.

The year 2026 marks a pivotal moment for estate planning. The provisions of the Tax Cuts and Jobs Act (TCJA) of 2017, which significantly increased the federal estate tax exemption, are set to expire. This expiration will likely lead to a substantial decrease in the exemption amount, meaning more estates will be subject to federal estate tax. For individuals and families with considerable assets, this impending change necessitates an immediate review and potential overhaul of existing estate plans. Our aim is to equip you with the knowledge and actionable strategies to navigate these changes, minimize tax liabilities, and secure your family’s financial future.

Effective estate tax planning 2026 involves a multi-faceted approach, combining legal, financial, and tax expertise. It’s about more than just drafting a will; it encompasses a wide array of tools and techniques designed to optimize wealth transfer while adhering to current and anticipated tax regulations. From understanding the nuances of gifting strategies to leveraging various types of trusts, each element plays a critical role in a robust estate plan. By adopting a proactive stance, you can transform potential tax burdens into opportunities for greater wealth preservation and intergenerational financial stability.

Understanding the Impending Changes in 2026 Estate Tax Exemptions

The foundation of any robust estate tax planning 2026 strategy begins with a clear understanding of the tax laws. The current federal estate tax exemption, which stands at $13.61 million per individual for 2024, is scheduled to revert to approximately $7 million (adjusted for inflation) on January 1, 2026. This significant reduction means that many more estates that were previously exempt will suddenly find themselves subject to the federal estate tax, which can be as high as 40%. This impending change underscores the urgency of reviewing and updating your estate plan.

The federal estate tax is levied on the transfer of a deceased person’s property and assets to their heirs. While most estates are not large enough to trigger this tax under current exemption levels, the 2026 reduction will bring a much larger segment of the population into its purview. It’s not just the ultra-wealthy who need to be concerned; even those with substantial homes, retirement accounts, and investment portfolios could find their estates facing significant tax liabilities. State estate taxes and inheritance taxes also play a role, further complicating the picture for residents in certain states. Therefore, a comprehensive strategy must consider both federal and state regulations.

For married couples, the exemption is effectively doubled, allowing for the transfer of a much larger sum without incurring federal estate tax. However, careful planning, often involving portability elections, is necessary to ensure both exemptions are fully utilized. The concept of portability allows a surviving spouse to use any unused portion of their deceased spouse’s federal estate tax exemption. However, this is not automatic and requires a timely filed estate tax return (Form 706) even if no tax is due. Failing to make this election can result in a significant loss of exemption for the surviving spouse, making meticulous estate tax planning 2026 even more critical.

Beyond the federal exemption, several states impose their own estate or inheritance taxes. These state-level taxes often have lower exemption thresholds than the federal government and can significantly impact the net inheritance received by beneficiaries. For example, some states have estate tax exemptions as low as $1 million, while others impose inheritance taxes directly on the beneficiaries, with rates varying based on the relationship to the deceased. Understanding the interplay between federal and state tax laws is paramount to developing an effective strategy that minimizes the overall tax burden on your estate and heirs.

The uncertainty surrounding future legislative action also adds another layer of complexity. While the current law dictates a reversion of the exemption amounts, there’s always a possibility of further legislative changes before or after 2026. However, relying on potential future legislation is a risky strategy. The most prudent approach is to plan based on the known expiration and to implement strategies that are effective under both current and anticipated tax regimes. This proactive stance ensures that your estate plan remains resilient and adaptable to any future changes, providing peace of mind for you and your family.

Leveraging Gifting Strategies to Reduce Your Taxable Estate

One of the most effective and widely used strategies in estate tax planning 2026 is strategic gifting. By transferring assets out of your estate during your lifetime, you can reduce the overall value of your taxable estate, thereby lowering potential estate tax liabilities. The IRS provides several avenues for tax-free gifting, which, when utilized wisely, can significantly benefit your heirs.

Annual Gift Tax Exclusion

The annual gift tax exclusion allows you to give a certain amount of money or assets to as many individuals as you wish each year without incurring gift tax or using any of your lifetime exemption. For 2024, this exclusion is $18,000 per recipient. This means a married couple can collectively give $36,000 to each recipient annually. Over several years, this strategy can remove a substantial amount of wealth from your estate, tax-free. For instance, if you and your spouse have three children and five grandchildren, you could collectively gift $36,000 to each of the eight individuals each year, totaling $288,000 annually. This cumulative effect can be incredibly powerful in reducing the size of your taxable estate for estate tax planning 2026.

It’s important to understand that gifts made under the annual exclusion do not count against your lifetime gift tax exemption. This makes it an incredibly valuable tool for those looking to gradually reduce their estate size. However, for a gift to qualify for the annual exclusion, it must be a ‘present interest’ gift, meaning the recipient must have immediate use, possession, and enjoyment of the gifted property. Gifts to trusts, for example, may require specific provisions (like ‘Crummey’ powers) to qualify for this exclusion.

Lifetime Gift Tax Exemption

Beyond the annual exclusion, you also have a lifetime gift tax exemption, which mirrors the federal estate tax exemption. For 2024, this is $13.61 million per individual. Any gifts made above the annual exclusion amount will begin to use up your lifetime exemption. While these gifts are not immediately taxed, they reduce the amount of your estate tax exemption available at death. Given the scheduled reduction in the exemption amount in 2026, making larger gifts now, while the exemption is higher, can be a highly advantageous strategy for estate tax planning 2026.

This strategy is particularly appealing for individuals who anticipate their estate will exceed the lower 2026 exemption amount. By making substantial gifts now, you ‘lock in’ the higher exemption. If the exemption amount does indeed revert in 2026, the gifts made under the higher exemption will generally not be clawed back into your estate for tax purposes, provided they were properly executed. This makes current large-scale gifting a powerful tool for proactive wealth transfer.

Paying for Education and Medical Expenses Directly

Another often-overlooked gifting strategy involves directly paying for certain expenses. Payments made directly to an educational institution for tuition (not room and board, books, or other fees) on behalf of another person, or directly to a medical provider for medical care, are not considered taxable gifts and do not count against your annual exclusion or lifetime exemption. This can be an excellent way to support family members while simultaneously reducing your estate. For instance, paying for a grandchild’s college tuition or a loved one’s significant medical bills can significantly benefit them without any gift tax implications, freeing up more of your estate for other beneficiaries.

These payments must be made directly to the institution or provider, not to the individual. If you give money to a family member who then pays their tuition or medical bills, that gift would count towards your annual exclusion. The direct payment method is a powerful, tax-efficient way to provide substantial financial support and is an integral part of comprehensive estate tax planning 2026.

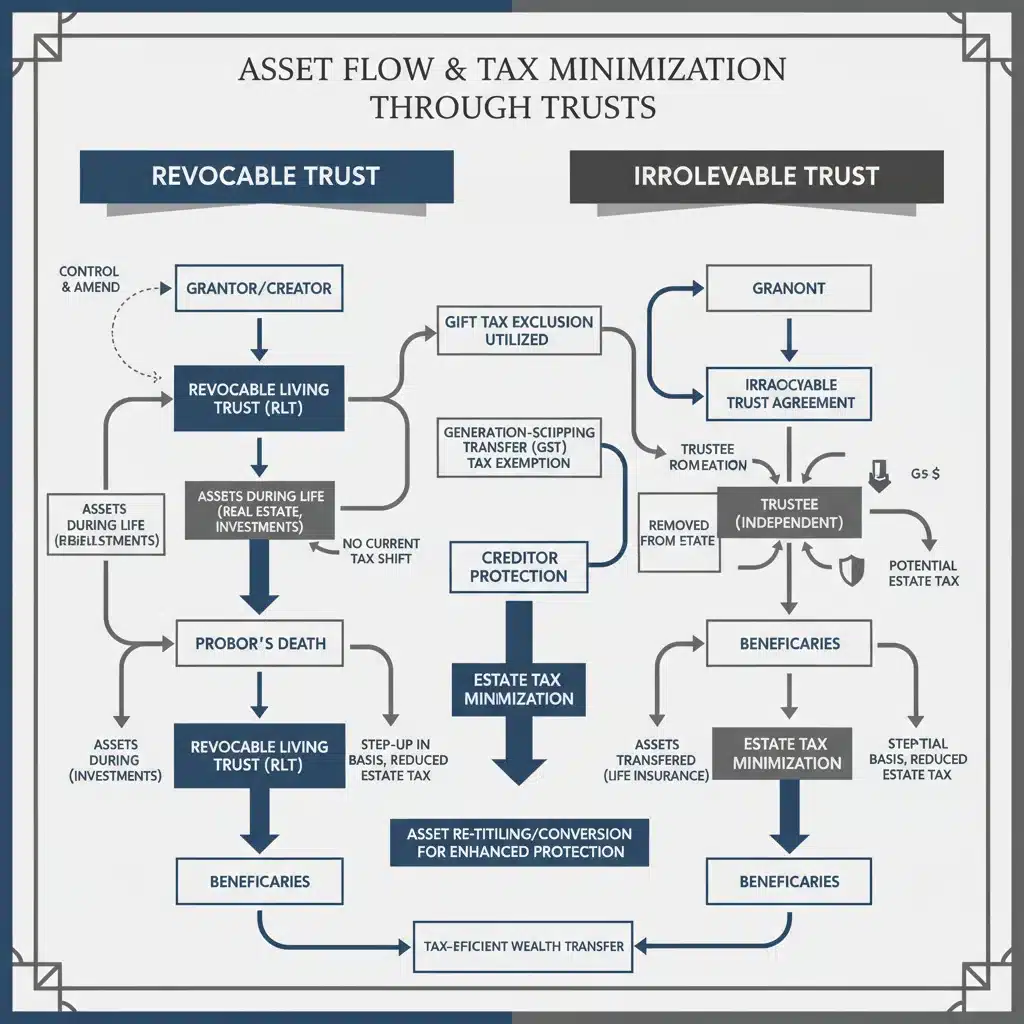

The Power of Trusts in 2026 Estate Tax Planning

Trusts are incredibly versatile tools in estate tax planning 2026, offering a wide range of benefits beyond simply avoiding probate. They can be instrumental in protecting assets, providing for beneficiaries with special needs, and most importantly, significantly reducing estate tax liabilities. Understanding the different types of trusts and how they can be applied is key to optimizing your estate plan.

Irrevocable Trusts

Irrevocable trusts are a cornerstone of advanced estate tax planning. Once assets are transferred into an irrevocable trust, they are generally removed from your taxable estate. This means that the assets, along with any future appreciation, will not be subject to estate taxes upon your death. The trade-off is that you typically give up control over the assets once they are placed in an irrevocable trust. However, various types of irrevocable trusts offer flexibility and can be tailored to specific needs.

- Irrevocable Life Insurance Trusts (ILITs): An ILIT is specifically designed to own a life insurance policy. By having the trust own the policy, the death benefit is excluded from your taxable estate. The trustee of the ILIT uses the death benefit to provide liquidity to your estate (e.g., to pay estate taxes) or to directly benefit your heirs, all outside of your taxable estate. This is a highly effective way to create a tax-free pool of funds for your beneficiaries.

- Grantor Retained Annuity Trusts (GRATs): GRATs allow you to transfer appreciating assets out of your estate while retaining an income stream (annuity) for a specified term. At the end of the term, any appreciation in the assets above a certain IRS-defined rate passes to your beneficiaries free of gift and estate tax. This strategy is particularly effective in a low-interest-rate environment and for assets expected to grow significantly.

- Charitable Lead Trusts (CLTs) and Charitable Remainder Trusts (CRTs): These trusts combine philanthropic goals with estate tax reduction. A CLT provides an income stream to a charity for a period, with the remaining assets passing to non-charitable beneficiaries (e.g., family) free of estate tax. A CRT, conversely, provides an income stream to non-charitable beneficiaries for a period, with the remainder going to charity. Both can offer significant tax advantages depending on your goals.

Dynasty Trusts

For those looking to preserve wealth across multiple generations, a dynasty trust (also known as a generation-skipping trust) is an invaluable tool. Assets placed in a dynasty trust can grow and be distributed to beneficiaries for many generations without being subject to estate or generation-skipping transfer (GST) taxes at each generation’s passing. This allows for the perpetual preservation of wealth, shielded from subsequent estate taxes, assuming the trust is structured correctly and complies with the rule against perpetuities (where applicable).

A key aspect of a dynasty trust is the use of the Generation-Skipping Transfer (GST) tax exemption. This exemption, which mirrors the federal estate tax exemption, allows you to transfer assets to grandchildren or more remote descendants without incurring the GST tax. Given the potential reduction in exemption amounts in 2026, utilizing your GST exemption now to fund a dynasty trust can be a very powerful strategy to lock in the higher exemption and secure multi-generational wealth transfer.

Qualified Personal Residence Trusts (QPRTs)

A Qualified Personal Residence Trust (QPRT) allows you to transfer your primary residence or a vacation home out of your taxable estate at a reduced gift tax value. You retain the right to live in the home for a specified term. At the end of the term, the home passes to your beneficiaries. If you outlive the term, the home and its future appreciation are removed from your estate. This strategy is particularly effective for high-value real estate that is expected to appreciate further, significantly reducing the taxable value of a major asset in your estate.

The gift tax value of the home is discounted because you retain the right to live in it for a period. This discount is calculated based on IRS actuarial tables. If you die before the term ends, the full value of the home would be included in your estate, so there is a mortality risk. However, for those in good health, a QPRT can be a very effective way to transfer significant real estate wealth with minimal gift and estate tax consequences as part of robust estate tax planning 2026.

Strategic Asset Valuation and Discounting

Beyond direct gifting and trusts, advanced estate tax planning 2026 often involves strategies related to asset valuation and discounting. These techniques aim to reduce the taxable value of assets transferred to heirs, thereby lowering the overall estate tax burden. These strategies are particularly relevant for business owners and those with illiquid assets.

Family Limited Partnerships (FLPs) and Limited Liability Companies (LLCs)

FLPs and LLCs are powerful tools for holding family assets, such as real estate, businesses, or investment portfolios. By transferring assets into an FLP or LLC and then gifting or selling interests in the entity to family members, you can achieve significant estate tax savings through valuation discounts. These discounts typically arise from two main factors:

- Lack of Marketability Discount: Interests in privately held entities are generally difficult to sell compared to publicly traded stocks. This illiquidity justifies a discount in their valuation for gift and estate tax purposes.

- Lack of Control Discount: Minority interests in an FLP or LLC typically do not confer control over the entity’s operations or distributions. This lack of control further justifies a discount in their valuation.

These discounts can be substantial, often ranging from 20% to 40% or more, allowing you to transfer a larger economic value of assets to your heirs while using less of your gift and estate tax exemption. However, the IRS closely scrutinizes FLPs and LLCs, so they must be properly structured and operated with a legitimate non-tax business purpose to withstand challenge.

Valuation of Business Interests

For business owners, the valuation of their business can be a critical component of estate tax planning 2026. Proper valuation, often conducted by qualified appraisers, can ensure that business interests are transferred at their fair market value, potentially leading to lower estate tax liabilities. Strategies such as gifting minority interests, implementing buy-sell agreements, or structuring the business for philanthropic giving can further optimize tax outcomes.

Buy-sell agreements, for example, can establish a predetermined value for a business interest upon a triggering event like death, which can be crucial for estate tax purposes. Properly drafted agreements can help lock in a lower, acceptable valuation for estate tax calculations, preventing disputes with the IRS over the value of a closely held business. This level of foresight is invaluable for seamless wealth transfer.

Charitable Giving as an Estate Tax Planning Strategy

For those with philanthropic inclinations, charitable giving can be an excellent way to reduce estate taxes while supporting causes you care about. When structured correctly, charitable contributions can provide significant income, gift, and estate tax benefits. Integrating charitable giving into your estate tax planning 2026 can be a win-win strategy.

Bequests in Your Will or Trust

The simplest form of charitable giving in estate planning is a direct bequest in your will or living trust. Any assets left to a qualified charity are entirely deductible from your taxable estate, reducing the overall estate tax burden. This can be a specific dollar amount, a percentage of your estate, or specific assets. Bequests are straightforward and ensure that your philanthropic wishes are honored while providing a valuable estate tax deduction.

Donor-Advised Funds (DAFs)

Donor-Advised Funds (DAFs) offer a flexible and tax-efficient way to manage your charitable giving. You contribute assets to a DAF, receive an immediate income tax deduction, and then recommend grants to your favorite charities over time. While the primary benefit of a DAF is the income tax deduction, it can also play a role in estate planning. Assets transferred to a DAF are generally removed from your taxable estate, and you can name successor advisors to continue your philanthropic legacy for generations without incurring additional estate tax.

Charitable Remainder Trusts (CRTs)

As mentioned earlier, CRTs allow you to donate assets to a trust, receive an income stream for a specified term or for life, and then have the remainder go to charity. The act of creating a CRT provides an immediate income tax deduction, and the assets transferred to the CRT are removed from your taxable estate. This strategy is particularly attractive for appreciated assets, as the CRT can sell the assets without incurring capital gains tax, allowing for a larger principal to generate income. This dual benefit of income stream and estate tax reduction makes CRTs a powerful tool for estate tax planning 2026.

Charitable Lead Trusts (CLTs)

Conversely, CLTs provide an income stream to a charity for a period, with the remaining assets eventually passing to non-charitable beneficiaries (e.g., family members). This can be a powerful estate tax reduction strategy, especially if the assets are expected to appreciate significantly. The present value of the income stream paid to the charity is deductible for gift or estate tax purposes, effectively reducing the taxable transfer to your heirs. CLTs are often used by individuals with large estates who wish to benefit charity while also passing assets to future generations with reduced tax liabilities.

Reviewing and Updating Beneficiary Designations

While often overlooked, correctly reviewing and updating beneficiary designations on retirement accounts, life insurance policies, and annuities is a fundamental aspect of effective estate tax planning 2026. These assets typically pass directly to the named beneficiaries, bypassing your will and often probate. However, improper or outdated designations can lead to unintended consequences, including significant tax burdens and assets going to the wrong people.

For retirement accounts like IRAs and 401(k)s, naming an individual beneficiary can lead to different tax outcomes compared to naming a trust or your estate. The SECURE Act of 2019 significantly altered the rules for inherited IRAs, generally requiring non-spouse beneficiaries to withdraw all assets within 10 years, accelerating tax obligations. Strategic beneficiary planning, potentially involving conduit trusts or accumulation trusts, can help manage these distributions and minimize tax impact for heirs. For example, a ‘stretch IRA’ strategy, which allowed beneficiaries to stretch distributions over their lifetime, is largely gone for most non-spouse beneficiaries, making careful planning even more vital.

Life insurance policies also have a unique role in estate planning. While the death benefit is generally income tax-free to the beneficiary, if you own the policy, the death benefit will be included in your taxable estate. As discussed, an Irrevocable Life Insurance Trust (ILIT) can own the policy, thus removing the death benefit from your estate. However, even without an ILIT, ensuring the correct beneficiary is named is crucial to prevent the proceeds from being tied up in probate or going to an unintended recipient. Regularly reviewing these designations is a simple yet powerful step in comprehensive estate tax planning 2026.

It’s not uncommon for individuals to forget to update beneficiaries after major life events such as marriage, divorce, birth of children, or death of a loved one. An outdated beneficiary designation could mean that an ex-spouse inherits assets, or that minor children receive funds outright without proper guardianship, or that assets become part of your probate estate, potentially subject to delays and additional taxes. Make it a routine practice to review all beneficiary designations at least every few years, and especially in light of the upcoming 2026 tax changes.

Considering Domicile and State Estate Taxes

Your legal domicile, or permanent home, plays a significant role in estate tax planning 2026, particularly concerning state estate and inheritance taxes. While the federal estate tax applies uniformly across the U.S. (subject to exemption amounts), many states impose their own estate or inheritance taxes, often with much lower exemption thresholds. These state-level taxes can add a substantial burden to your heirs, sometimes exceeding the federal tax impact for estates just above state exemptions.

Currently, about 12 states and the District of Columbia levy an estate tax, and 6 states levy an inheritance tax. Some states impose both. The rules vary dramatically, with exemptions ranging from $1 million to the federal exemption amount. For example, Oregon and Massachusetts have estate tax exemptions of $1 million, meaning estates valued over this amount will be subject to state estate tax. New Jersey, on the other hand, has an inheritance tax where the tax rate depends on the beneficiary’s relationship to the deceased. This can lead to beneficiaries paying a percentage of their inheritance directly, in addition to any federal estate taxes on the overall estate.

If you own property in multiple states, or if you are considering a move, understanding the domicile rules and state-specific estate tax laws is critical. Some states have very strict rules for determining domicile, and merely owning a vacation home or having a driver’s license in a different state may not be enough to change your legal residence. A change in domicile could potentially save your estate significant amounts in state-level estate taxes, but it requires careful planning and establishing clear ties to the new state of residence.

For individuals with substantial assets residing in states with high estate taxes, exploring a change of domicile to a state with no estate or inheritance tax (e.g., Florida, Texas, Nevada) can be a highly effective strategy. This decision, however, should not be taken lightly and involves a comprehensive review of all personal and financial factors. It requires establishing genuine residency in the new state, including registering to vote, obtaining a driver’s license, filing state income taxes there, and spending a significant amount of time in the new location. Consulting with an attorney specializing in multi-state estate planning is essential to navigate these complexities and ensure compliance.

The Importance of Professional Guidance for 2026 Estate Tax Planning

Navigating the complex world of estate tax laws, especially with the impending changes in 2026, is not a DIY project. The potential for costly mistakes, missed opportunities, and unintended tax consequences is too high. Engaging experienced professionals is not just advisable; it’s essential for effective estate tax planning 2026.

Estate Planning Attorneys

An estate planning attorney is crucial for drafting legally sound documents such as wills, trusts, and powers of attorney. They ensure that your documents comply with all federal and state laws and are tailored to your specific goals and family situation. They can advise on the legal implications of various strategies, help structure trusts, and ensure assets are properly titled to align with your estate plan. Their expertise is invaluable in avoiding common pitfalls and ensuring your wishes are legally enforceable.

Financial Advisors

A financial advisor plays a key role in integrating your estate plan with your broader financial goals. They can help assess your current asset allocation, project future growth, and determine the potential size of your taxable estate. They can also advise on investment strategies that complement your estate plan, such as funding trusts or optimizing portfolios for legacy transfer. A good financial advisor works in tandem with your estate attorney to ensure all financial aspects are aligned with your legal documents.

Tax Professionals (CPAs or Tax Attorneys)

Given the primary focus on tax reduction, a tax professional is an indispensable member of your estate planning team. They can provide detailed analysis of current and future tax liabilities, advise on the tax implications of various gifting and trust strategies, and ensure all tax filings are accurate and timely. They stay abreast of legislative changes and can help you adapt your plan to optimize for tax efficiency, particularly with the 2026 changes looming. Their expertise can help quantify the potential savings and guide decisions on the most tax-advantageous approaches.

Regular Review and Adjustments

Estate planning is not a one-time event; it’s an ongoing process. Life circumstances change, family dynamics evolve, and tax laws are consistently updated. With the significant changes anticipated in 2026, it is more critical than ever to regularly review and, if necessary, adjust your estate plan. We recommend reviewing your plan every 3-5 years, or immediately following any major life event (marriage, divorce, birth, death, significant inheritance, sale of a business, etc.). A proactive approach to reviewing your estate tax planning 2026 ensures it remains aligned with your goals and is optimized for the current legal and tax environment.

Conclusion: Act Now for Optimal Estate Tax Planning 2026

The impending changes to federal estate tax exemptions in 2026 present both challenges and opportunities for wealth transfer. The potential reduction in the exemption amount means that many more estates will be subject to federal estate tax, making proactive and strategic estate tax planning 2026 more critical than ever before. By understanding the nuances of these changes and implementing smart strategies, you have the power to significantly reduce your heirs’ tax burden, potentially by up to 40% or more, and ensure your legacy is preserved for future generations.

From leveraging annual and lifetime gifting exclusions to establishing sophisticated trust structures like ILITs, GRATs, and dynasty trusts, the tools available for effective estate tax reduction are numerous. Strategic asset valuation, including the use of FLPs and LLCs, can further reduce the taxable value of your estate. Incorporating charitable giving can also align your philanthropic goals with substantial tax benefits. Moreover, meticulous attention to beneficiary designations and understanding the impact of state-specific estate taxes are vital components of a comprehensive plan.

The most important takeaway is the urgency of action. Waiting until 2026 or later could mean missing out on valuable opportunities to utilize higher exemption amounts and implement strategies that take time to mature. Engage with a team of qualified professionals – an estate planning attorney, financial advisor, and tax professional – to review your current situation, assess potential liabilities, and craft a tailored plan. Regular review and adjustment of your plan will ensure it remains robust and responsive to changes in your life and in the tax landscape.

Don’t let the complexities of estate tax laws diminish your legacy. Take control of your financial future and empower your heirs by acting now. Proactive estate tax planning 2026 is the key to ensuring your wealth is transferred efficiently, securely, and with the greatest benefit to your loved ones. Start the conversation with your advisors today and build a plan that truly reflects your wishes and safeguards your family’s prosperity for years to come.