Debt Consolidation 2025: Reduce Payments, Accelerate Freedom

Debt consolidation in 2025 provides streamlined approaches to combine multiple high-interest debts into a single, lower monthly payment, effectively reducing financial burdens and accelerating debt repayment.

Are you feeling overwhelmed by multiple monthly debt payments and high-interest rates? Debt consolidation in 2025 could be the strategic financial move you need to gain control, simplify your finances, and potentially reduce your monthly payments by 10-15%, paving the way for accelerated financial freedom.

Understanding debt consolidation in 2025

Debt consolidation involves combining several debts, often high-interest ones like credit card balances or personal loans, into a single, new loan or payment plan. The primary goal is to simplify your financial obligations and, ideally, secure a lower interest rate or a more manageable monthly payment.

In 2025, the financial landscape continues to evolve, bringing new opportunities and considerations for those looking to consolidate debt. Interest rates, economic stability, and lender offerings can all impact the effectiveness of a consolidation strategy. Understanding these factors is crucial for making an informed decision that aligns with your long-term financial goals.

The core benefit remains the same: transforming several disparate payments into one, making budgeting easier and reducing the risk of missed payments. However, the specific tools and optimal approaches for achieving this in the current year require a fresh perspective.

Ultimately, a successful debt consolidation plan in 2025 is not just about reducing payments; it’s about creating a sustainable path to becoming debt-free and building a stronger financial foundation for the future.

Key benefits of consolidating your debt

The advantages of debt consolidation extend beyond simply reducing your monthly outflow. It offers a holistic approach to debt management that can significantly improve your financial well-being and accelerate your journey toward financial independence.

One of the most immediate benefits is the simplification of your finances. Instead of tracking multiple due dates and minimum payments, you’ll have just one to remember, reducing stress and the likelihood of late fees. This streamlined approach allows for clearer budgeting and better oversight of your financial progress.

Lowering interest rates and monthly payments

Perhaps the most compelling benefit is the potential to secure a lower interest rate. High-interest debts, such as credit card balances, can make it feel like you’re constantly treading water. By consolidating, you might qualify for a new loan with a significantly lower Annual Percentage Rate (APR), which directly translates to:

- Reduced overall cost of your debt.

- A larger portion of your payment going towards the principal.

- Faster debt repayment.

This reduction in interest can free up a substantial amount of money each month, which can then be used to pay down the principal even faster, save for emergencies, or invest in your future.

Improving your credit score over time

While the immediate impact on your credit score can vary, successful debt consolidation often leads to long-term improvements. By making consistent, on-time payments on your new consolidated loan, you demonstrate responsible financial behavior. Furthermore, consolidating credit card debt can lower your credit utilization ratio, a key factor in credit scoring.

It’s important to monitor your credit score throughout the process and avoid taking on new debt. The goal is to close the chapter on old debts and build a positive payment history with your consolidated loan.

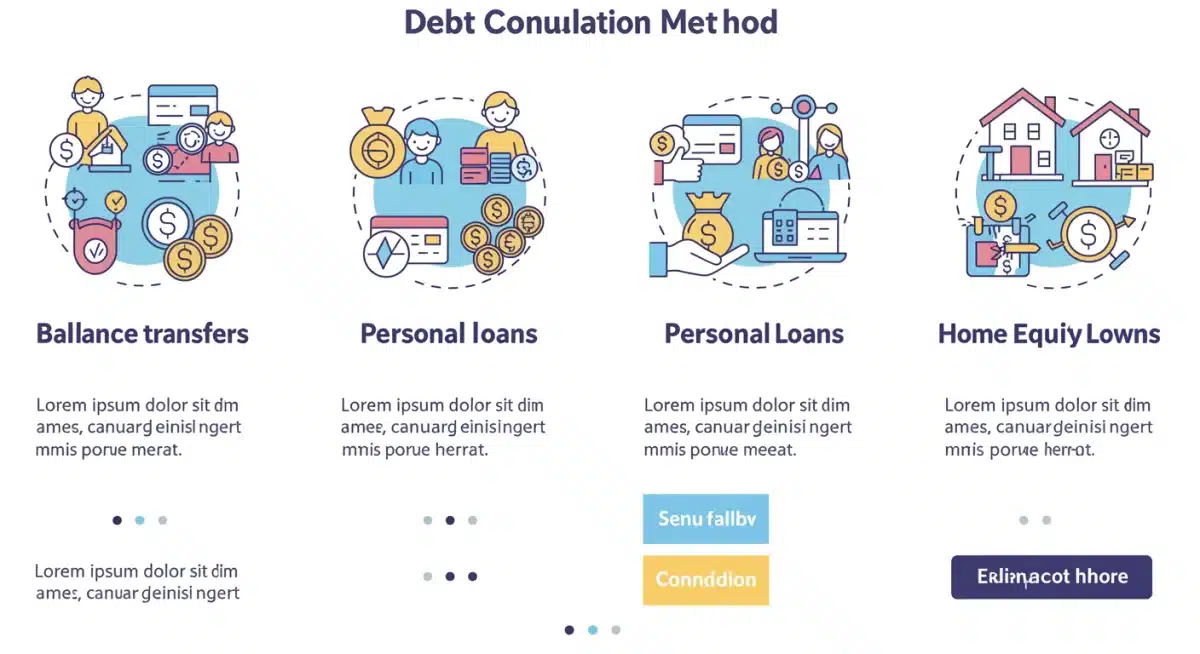

Common debt consolidation methods for 2025

In 2025, several proven methods for debt consolidation remain popular, each with its own set of advantages and considerations. Choosing the right method depends on your credit score, the amount of debt you have, and your financial goals.

It’s crucial to evaluate each option carefully and understand how it aligns with your personal financial situation. Consulting with a financial advisor can also provide valuable insights into which method might be best for you.

Understanding the nuances of each option is key to making an informed decision that truly helps you achieve financial freedom.

Balance transfer credit cards

A balance transfer credit card allows you to move high-interest debt from one or more credit cards to a new card, often with a promotional 0% APR for an introductory period (typically 6 to 21 months). This can be an excellent option if you have good credit and are confident you can pay off the transferred balance before the promotional period ends.

- Pros: Potential for 0% interest for a significant period, allowing you to pay down principal quickly.

- Cons: Balance transfer fees (typically 3-5% of the transferred amount), high interest rates after the promotional period, and the temptation to incur new debt on old cards.

This method requires discipline and a clear repayment plan to be effective. Failure to pay off the balance within the introductory period can lead to higher interest rates than your original debt.

Personal loans for debt consolidation

A personal loan is an unsecured loan you can use for various purposes, including debt consolidation. If you have good credit, you might qualify for a personal loan with a fixed interest rate lower than what you’re paying on your credit cards. This provides a predictable monthly payment and a clear end date for your debt.

- Pros: Fixed interest rates and payments, clear repayment schedule, no collateral required.

- Cons: Eligibility depends on credit score and income, interest rates can still be high for those with less-than-perfect credit.

Many lenders offer personal loans specifically for debt consolidation, making it a popular choice for many individuals seeking to streamline their finances.

Home equity loans and lines of credit (HELOCs)

If you own a home, you might consider using your home’s equity to consolidate debt. A home equity loan provides a lump sum, while a home equity line of credit (HELOC) works like a revolving credit line. Both typically offer lower interest rates than unsecured loans because your home serves as collateral.

- Pros: Lower interest rates, potential tax deductibility of interest (consult a tax professional), larger loan amounts.

- Cons: Your home is used as collateral, meaning you risk foreclosure if you can’t make payments.

This option carries significant risk and should be approached with extreme caution, especially if your job security or income is uncertain.

Strategic planning for successful debt consolidation

Successful debt consolidation is not merely about choosing a method; it requires careful planning and a commitment to financial discipline. Without a solid strategy, you risk falling back into debt or even worsening your situation.

Start by honestly assessing your current financial situation. This includes a detailed review of all your debts, their interest rates, and your monthly income and expenses. A clear picture of your finances is the first step toward effective planning.

Assessing your current financial situation

Before considering any consolidation option, accurately list all your debts: credit cards, personal loans, medical bills, and any other unsecured debts. Note the outstanding balance, interest rate, and minimum monthly payment for each. This comprehensive overview will help you understand the total scope of your debt and identify which high-interest accounts to prioritize.

Also, review your monthly budget to understand your income and expenses. Identify areas where you can cut back to free up more money for debt repayment. A realistic budget is crucial for ensuring you can comfortably afford your new consolidated payment.

Creating a realistic budget and repayment plan

Once you’ve consolidated your debt, it’s paramount to stick to a strict budget and a clear repayment plan. Your consolidated payment should be manageable within your monthly income. If it’s not, you might need to reconsider the loan terms or look for ways to increase your income or reduce expenses further.

Consider setting up automatic payments to avoid missing due dates. Aim to pay more than the minimum whenever possible to accelerate your debt repayment and save on interest. The goal is not just to consolidate but to eliminate the debt entirely.

Avoiding new debt after consolidation

One of the biggest pitfalls after consolidating debt is accumulating new debt. It’s essential to address the underlying spending habits that led to debt in the first place. This might involve closing old credit card accounts (though be mindful of the immediate impact on your credit score) or developing healthier financial habits.

Focus on living within your means and building an emergency fund to prevent future reliance on credit for unexpected expenses. Debt consolidation is a fresh start; protect it by committing to responsible spending.

The role of credit scores in debt consolidation

Your credit score plays a pivotal role in determining your eligibility for various debt consolidation options and the interest rates you’ll receive. A higher credit score generally translates to better loan terms, which can significantly impact the effectiveness and cost of your consolidation strategy.

Lenders use your credit score as an indicator of your creditworthiness. It tells them how likely you are to repay your debts. Therefore, understanding your credit score and taking steps to improve it can be a crucial part of your debt consolidation journey.

How credit scores impact loan offers

When applying for a balance transfer card, personal loan, or home equity loan, lenders will review your credit report and score. A strong credit score (typically FICO scores above 670) can help you qualify for lower interest rates, higher loan amounts, and more favorable terms. Conversely, a lower credit score might lead to higher interest rates, smaller loan offers, or even rejection.

It’s advisable to check your credit score and report before applying for any consolidation product. This allows you to identify any errors and understand where you stand. You can obtain a free credit report once a year from each of the three major credit bureaus: Equifax, Experian, and TransUnion.

Tips for improving your credit score

If your credit score isn’t where you’d like it to be, there are steps you can take to improve it before applying for debt consolidation:

- Pay bills on time: Payment history is the most significant factor in your credit score.

- Reduce credit utilization: Keep your credit card balances low relative to your credit limits.

- Avoid opening new credit accounts: Each new application can temporarily ding your score.

- Review your credit report for errors: Dispute any inaccuracies immediately.

Even a modest improvement in your credit score can lead to better consolidation offers, potentially saving you thousands of dollars in interest over the life of the loan.

Navigating potential challenges and pitfalls

While debt consolidation offers a promising path to financial relief, it’s not without its challenges. Being aware of potential pitfalls can help you avoid them and ensure your consolidation strategy leads to genuine financial improvement.

One common mistake is viewing consolidation as a quick fix without addressing the root causes of debt. Without a change in spending habits, new debt can quickly accumulate, leaving you in a worse position than before.

Understanding fees and hidden costs

Many consolidation options come with fees that can add to the overall cost. Balance transfer cards often have balance transfer fees, personal loans may have origination fees, and home equity loans can involve closing costs. Always read the fine print and ask about all associated fees before committing to a loan.

These fees can sometimes negate the benefit of a lower interest rate, especially for smaller loan amounts or shorter repayment periods. Factor all costs into your calculations to get an accurate picture of the total expense.

The risk of increased debt

Perhaps the most significant risk is falling back into debt, or even accumulating more. When you consolidate, your old credit accounts might become available again. If you haven’t changed your spending habits, you might be tempted to use them, leading to a situation where you have both the consolidated loan and new credit card debt.

To mitigate this risk, consider closing the old credit card accounts once the balances are transferred. For those who need to maintain a few credit lines, commit to using them responsibly and paying off balances in full each month.

Impact on credit score (short-term vs. long-term)

In the short term, applying for a new loan or credit card for consolidation can temporarily lower your credit score due to a hard inquiry. Additionally, closing old accounts can reduce your overall available credit, which might also impact your score. However, these effects are usually temporary.

Long-term, successfully managing your consolidated debt and making consistent, on-time payments will positively impact your credit score. The key is to see consolidation through to completion and maintain responsible credit behavior afterward.

Achieving financial freedom with debt consolidation

The ultimate goal of debt consolidation is not just to manage debt, but to eliminate it and achieve lasting financial freedom. With careful planning and disciplined execution, consolidation can be a powerful tool to transform your financial future in 2025.

By reducing your interest payments and simplifying your financial obligations, you free up resources and mental energy to focus on building wealth and securing your financial independence.

Long-term financial planning beyond debt

Once your debt is under control, shift your focus to long-term financial planning. This includes building a robust emergency fund, setting up retirement savings, and exploring investment opportunities. The money saved on interest payments can now be redirected towards these wealth-building goals.

Consider consulting with a financial advisor to create a comprehensive long-term plan that aligns with your aspirations. This proactive approach will help you stay on track and make the most of your newfound financial flexibility.

Maintaining financial discipline and healthy habits

Financial freedom is a journey, not a destination. It requires continuous discipline and the cultivation of healthy financial habits. Regularly review your budget, monitor your spending, and avoid taking on unnecessary debt.

Educate yourself on personal finance topics, stay informed about economic trends, and make informed decisions that support your financial well-being. The habits you build during and after debt consolidation will be crucial for maintaining your financial health for years to come.

| Key Point | Brief Description |

|---|---|

| Simplify Payments | Combines multiple debts into one manageable monthly payment. |

| Reduce Interest | Potential for lower overall interest rates, saving money. |

| Improve Credit | Consistent payments can positively impact credit score over time. |

| Avoid New Debt | Crucial to address spending habits to prevent re-accumulation of debt. |

Frequently asked questions about debt consolidation

Debt consolidation combines multiple debts into a single, new loan, often with a lower interest rate or more favorable terms. This simplifies payments and can reduce your overall monthly financial burden, making it easier to manage and pay off debt.

By securing a new loan with a lower interest rate or a longer repayment term, debt consolidation can significantly decrease your total monthly payment. This reduction frees up cash flow, making your budget more manageable and your debt repayment journey more achievable.

Common methods include balance transfer credit cards, personal loans, and home equity loans or lines of credit (HELOCs). Each option has unique eligibility requirements, interest rates, and risks, so careful consideration is essential for choosing the best fit.

Initially, applying for new credit can cause a temporary dip due to a hard inquiry. However, successful debt consolidation, along with consistent, on-time payments and reduced credit utilization, can lead to significant long-term improvements in your credit score.

After consolidating, focus on sticking to your new repayment plan, avoid taking on new debt, and cultivate healthy financial habits. Consider closing old credit accounts and building an emergency fund to prevent future reliance on credit and secure your financial future.

Conclusion

Debt consolidation in 2025 stands as a powerful tool for individuals seeking to simplify their finances, reduce monthly payments, and accelerate their journey toward financial freedom. By strategically combining multiple debts into one, you can gain better control over your financial health. Success hinges on careful planning, understanding the available methods, and a steadfast commitment to responsible financial habits. Embrace this opportunity to transform your debt burden into a clear path to lasting financial stability and peace of mind.

")