2026 Housing Market Forecast: Affordability Shifts & Key Trends

The 2026 Housing Market: Navigating Supply, Demand, and a Projected 4% Shift in Affordability

The housing market is a dynamic and ever-evolving entity, constantly shaped by a confluence of economic, social, and demographic factors. As we cast our gaze forward to 2026, the landscape appears poised for significant shifts, particularly concerning supply, demand, and, most notably, affordability. For potential homebuyers, sellers, investors, and industry professionals alike, understanding these projected changes is not just beneficial but essential for strategic planning and informed decision-making. This comprehensive analysis delves deep into the anticipated trends of the 2026 Housing Market, examining the forces at play and offering insights into what lies ahead.

The past few years have been a rollercoaster for real estate, marked by unprecedented demand, historically low interest rates, and soaring prices, followed by a period of recalibration. As we approach 2026, many of these existing trends will continue to evolve, while new challenges and opportunities emerge. A key projection indicates a notable 4% shift in affordability, a metric that will undoubtedly influence buying power and market accessibility. This shift is not a standalone event but rather a symptom of broader economic currents, including inflation, interest rate adjustments, and the ongoing struggle between housing supply and persistent demand.

Our exploration will cover the intricate dance between housing supply and buyer demand, dissecting the underlying causes of current imbalances and forecasting their trajectory. We will also scrutinize the critical role of interest rates and inflation, two powerful economic levers that directly impact mortgage costs and, consequently, affordability. Furthermore, we will consider the impact of demographic shifts, evolving consumer preferences, and technological advancements on the future of housing. By the end of this article, readers should have a clearer picture of the challenges and opportunities that the 2026 Housing Market will present, enabling them to navigate this complex environment with greater confidence.

Understanding the Core Dynamics: Supply and Demand in the 2026 Housing Market

The fundamental principles of supply and demand remain the bedrock of any market analysis, and the 2026 Housing Market is no exception. The imbalance between these two forces has been a defining characteristic of recent years, leading to rapid price appreciation and intense competition. Looking ahead, while some adjustments are expected, a perfect equilibrium is unlikely to be achieved, continuing to shape market dynamics.

The Supply Side: Persistent Shortages and Construction Challenges

Despite increased construction activity in some regions, the overall housing supply in many parts of the United States and other developed nations is still lagging behind demand. This deficit is not a recent phenomenon but a cumulative effect of underbuilding over the past decade following the 2008 financial crisis. Several factors contribute to this persistent shortage:

- Labor Shortages: The construction industry continues to grapple with a scarcity of skilled labor, which slows down building timelines and increases costs.

- Material Costs: Fluctuations in the cost of building materials, exacerbated by supply chain disruptions, add to the overall expense of new home construction, making it less profitable to build entry-level homes.

- Regulatory Hurdles and Zoning: Stringent zoning laws, lengthy permitting processes, and local opposition to new developments often impede the construction of diverse housing types, particularly denser, more affordable options.

- Land Availability and Cost: Developable land, especially in desirable urban and suburban areas, is becoming increasingly scarce and expensive, pushing up the final price of new homes.

- Existing Home Inventory: Many homeowners, especially those with historically low mortgage rates, are reluctant to sell, fearing they won’t be able to find a suitable replacement property or will face significantly higher financing costs. This “lock-in effect” further constrains the supply of existing homes on the market.

By 2026, while some of these pressures might ease slightly, a dramatic surge in supply sufficient to meet pent-up demand is improbable. We can anticipate continued efforts to streamline construction and encourage denser developments, but these are long-term solutions that will take time to significantly impact the overall supply picture. The 2026 Housing Market will likely still be characterized by limited inventory, particularly in sought-after locations.

The Demand Side: Demographic Tailwinds and Evolving Preferences

On the demand side, several powerful forces are expected to keep buyer interest robust, even in the face of affordability challenges:

- Millennial and Gen Z Homeownership: The largest demographic cohorts, Millennials and now Gen Z, are increasingly reaching prime homebuying age. Despite facing hurdles, the desire for homeownership remains strong, driven by aspirations for stability, wealth building, and family formation.

- Immigration: Net immigration continues to contribute to population growth, especially in urban centers and economic hubs, adding to the demand for housing.

- Household Formation: Even with smaller household sizes, the sheer number of new households being formed outstrips the rate of new construction, creating a persistent demand gap.

- Investor Activity: While potentially less frenzied than in peak boom periods, institutional and individual investors will likely continue to view real estate as a valuable asset class, contributing to demand, particularly in rental markets.

- Shifting Work Patterns: The increased prevalence of remote and hybrid work models has broadened the geographical scope for many homebuyers, creating demand in previously less popular areas. This decentralization could alleviate pressure in some major metros but intensify it in others.

The interplay of these factors suggests that while demand might temper from its most fervent peaks, it will remain a formidable force in the 2026 Housing Market. The challenge will be how this sustained demand interacts with the constrained supply, inevitably impacting prices and, crucially, affordability.

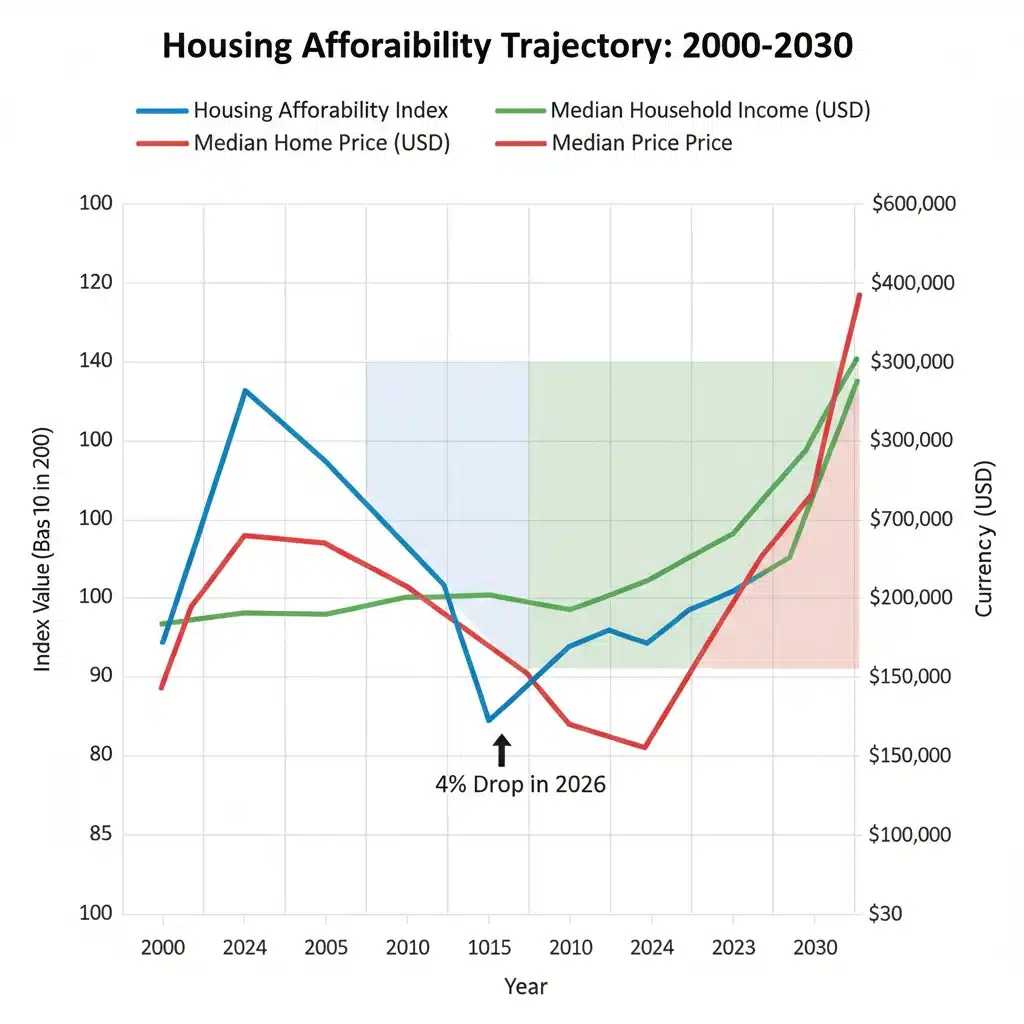

The Affordability Conundrum: A Projected 4% Shift

One of the most critical predictions for the 2026 Housing Market is a projected 4% shift in affordability. This figure, while seemingly modest, represents a significant hurdle for many prospective buyers and indicates a tightening of market access. Affordability is typically measured by the relationship between median home prices, median household incomes, and prevailing mortgage interest rates. A 4% shift means that, on average, a household’s ability to purchase a median-priced home will be 4% more challenging than it was in a preceding period, likely due to a combination of factors.

Factors Driving the Affordability Shift:

- Sustained High Home Prices: Despite some localized corrections, overall home prices are not expected to decline significantly across the board. Continued demand and limited supply will likely keep prices elevated, even if the rate of appreciation slows. This means the denominator in the affordability equation (home price) remains high.

- Interest Rate Environment: The era of ultra-low interest rates is likely behind us. While predicting exact rates for 2026 is challenging, the consensus points to rates remaining higher than the historical lows seen during the pandemic. Even small increases in mortgage rates can significantly impact monthly payments and, by extension, buying power. A 4% shift could easily be influenced by a quarter to half-point increase in mortgage rates over current levels, assuming other factors remain constant.

- Wage Growth vs. Inflation: While wage growth has been strong in some sectors, it has struggled to keep pace with the combined effects of housing price appreciation and broader inflation. If real wages (after accounting for inflation) stagnate or decline, purchasing power diminishes, contributing to the affordability gap.

- Down Payment Challenges: With higher home prices, the required down payment also increases, posing a significant barrier for first-time buyers who may struggle to save substantial sums.

- Increased Property Taxes and Insurance: As home values rise and climate-related risks become more pronounced, property taxes and home insurance premiums are also on an upward trend, adding to the overall cost of homeownership and further eroding affordability.

This 4% affordability shift in the 2026 Housing Market will have profound implications. It will likely push more potential buyers out of the market, particularly those at the lower end of the income spectrum or those without significant existing equity. It may also lead to a greater reliance on alternative financing options, or a longer period of saving for a down payment. For policymakers, it highlights the urgent need for solutions to address housing accessibility.

The Macroeconomic Landscape: Interest Rates, Inflation, and Economic Growth

The broader economic environment will play a pivotal role in shaping the 2026 Housing Market. Key macroeconomic indicators such as interest rates, inflation, and overall economic growth are intrinsically linked to housing market performance.

Interest Rates: The Dominant Lever

The Federal Reserve and other central banks use interest rates as a primary tool to manage inflation and stimulate or cool the economy. The rapid rate hikes of recent years have already had a significant cooling effect on housing demand. For 2026, while further aggressive hikes are less likely, a return to the near-zero rates of the past is also improbable. We can expect:

- Stabilized, Moderately Higher Rates: Interest rates are likely to stabilize at a level higher than the pandemic lows but potentially lower than their current peaks. This ‘new normal’ will still present a challenge for affordability compared to recent history.

- Impact on Mortgage Payments: Even a seemingly small percentage point difference in mortgage rates can translate into hundreds of dollars in monthly payments, directly affecting how much home a buyer can afford.

- Refinancing Activity: Higher rates will continue to deter refinancing activity, keeping more homeowners locked into their current loans.

Inflation: An Enduring Challenge

Persistent inflation, even if moderating, will continue to impact the 2026 Housing Market in several ways:

- Cost of Living: Higher costs for everyday goods and services reduce disposable income, making it harder for households to save for a down payment or manage increased mortgage payments.

- Construction Costs: Inflation directly affects the cost of labor and materials, contributing to higher new home prices and making it challenging for developers to build affordable housing.

- Rental Market Pressure: If homeownership becomes less accessible due to inflation and higher rates, more people will remain in the rental market, driving up rental costs and further straining household budgets.

Economic Growth and Employment

A strong labor market and sustained economic growth are generally positive for housing, as they support income growth and consumer confidence. However, if economic growth falters or if there’s a significant increase in unemployment, housing demand could soften more considerably. The 2026 Housing Market will be sensitive to global economic conditions and geopolitical stability, which can influence investment, trade, and overall consumer sentiment.

Demographic Shifts and Buyer Behavior in 2026

Beyond the raw numbers of supply and demand, the evolving characteristics of homebuyers and their preferences will also shape the 2026 Housing Market.

The Rise of Younger Generations

Millennials and Gen Z are not just entering the market; they are increasingly becoming the dominant force. Their preferences differ from previous generations:

- Sustainability and Technology: Younger buyers often prioritize energy-efficient homes, smart home technology, and properties with a lower environmental footprint.

- Walkability and Amenities: Access to amenities, public transportation, and walkable neighborhoods are often key considerations, especially for those in urban and suburban areas.

- Flexibility and Mixed-Use Spaces: The demand for homes that can accommodate remote work, home gyms, or multi-generational living is growing.

Multi-Generational Living and Smaller Households

The trend of multi-generational households is on the rise, driven by affordability concerns, cultural preferences, and caregiving needs. This creates demand for homes with separate living spaces, accessory dwelling units (ADUs), or flexible floor plans. Simultaneously, the average household size continues to shrink, leading to a greater number of households overall and a demand for smaller, more efficient living spaces.

Migration Patterns and Regional Differences

Post-pandemic migration patterns, particularly the movement away from expensive coastal cities to more affordable interior regions, are expected to continue, albeit potentially at a slower pace. This will create hot spots in some secondary and tertiary markets, driving up prices and potentially exacerbating local affordability challenges. The 2026 Housing Market will therefore be highly localized, with significant variations in conditions from one region to another.

The Role of Technology and Innovation

Technology continues to revolutionize the real estate industry, and its impact on the 2026 Housing Market will be profound.

- Artificial Intelligence and Data Analytics: AI-powered tools will become even more sophisticated in predicting market trends, valuing properties, and personalizing the home search experience. This will empower both buyers and sellers with more accurate and timely information.

- Virtual and Augmented Reality: Virtual tours and augmented reality tools will become standard, allowing buyers to experience properties remotely with greater immersion and detail, reducing the need for physical visits.

- Blockchain and Digital Transactions: While still in nascent stages for mainstream real estate, blockchain technology could streamline property transfers, enhance security, and reduce transaction costs in the future, potentially seeing more pilots and limited adoption by 2026.

- PropTech Innovations: The broader Property Technology (PropTech) sector will continue to introduce innovations in home construction (e.g., modular homes, 3D printing), property management, and smart home systems, all of which can influence supply, efficiency, and desirability.

These technological advancements will enhance efficiency and transparency but will also require the industry to adapt. Real estate professionals who embrace these tools will be better positioned to serve clients in the evolving 2026 Housing Market.

Navigating the 2026 Housing Market: Advice for Buyers, Sellers, and Investors

Given the projected trends, particularly the 4% shift in affordability, strategic planning will be paramount for all participants in the 2026 Housing Market.

For Prospective Buyers:

- Prioritize Financial Health: Strengthen your credit score, reduce debt, and save as large a down payment as possible. A solid financial foundation will be crucial in a less affordable market.

- Get Pre-Approved: Understand your true buying power by getting pre-approved for a mortgage early in your search. This clarifies your budget and makes your offer more attractive.

- Be Flexible: Consider alternative locations, smaller homes, or properties that might require some renovation. Flexibility can open up more affordable options.

- Explore First-Time Buyer Programs: Research local, state, and federal programs designed to assist first-time homebuyers, which can help with down payments or closing costs.

- Work with an Experienced Agent: A knowledgeable real estate agent can provide invaluable insights into local market conditions, identify opportunities, and help navigate complex transactions.

For Sellers:

- Price Strategically: While demand remains, the market may be less frenzied. Pricing your home competitively and realistically from the outset will be key to attracting buyers.

- Focus on Condition and Presentation: Homes that are well-maintained, updated, and staged effectively will stand out in a market where buyers are more discerning due to affordability constraints.

- Understand Your Local Market: Work with an agent who has a deep understanding of your specific neighborhood’s dynamics, as conditions can vary significantly even within the same city.

- Be Prepared for Negotiation: While bidding wars might still occur for highly desirable properties, sellers should be prepared for more negotiation on price and terms.

For Investors:

- Long-Term Vision: The 2026 Housing Market may favor long-term investment strategies over short-term flips, especially with higher interest rates impacting profitability.

- Focus on Cash Flow: Rental properties in areas with strong rental demand and favorable rent-to-price ratios will likely be attractive.

- Diversify Portfolios: Consider diversifying across different property types (single-family, multi-family, commercial) and geographic locations to mitigate risk.

- Monitor Economic Indicators: Keep a close eye on interest rates, inflation, and local economic growth to make informed investment decisions.

Policy Implications and Future Outlook

The projected 4% shift in affordability and the ongoing supply-demand imbalance in the 2026 Housing Market underscore the need for effective policy interventions. Governments at all levels will likely face increased pressure to address housing crises.

- Zoning Reform: Efforts to reform restrictive zoning laws to allow for denser, more diverse housing types (e.g., duplexes, townhouses, ADUs) are crucial.

- Incentives for Builders: Policies that incentivize the construction of affordable housing, reduce regulatory burdens, and support workforce development in the construction sector will be vital.

- First-Time Buyer Assistance: Expansion of down payment assistance programs, shared equity models, and other initiatives to help first-time buyers overcome affordability barriers.

- Investment in Infrastructure: Investing in infrastructure (transportation, utilities) can open up new areas for development and ease pressure on existing housing stock.

The 2026 Housing Market will not be a monolithic entity. It will be a patchwork of regional markets, each with its unique characteristics, influenced by local economies, demographics, and policy decisions. While the overarching trend points to continued affordability challenges, particularly with the projected 4% shift, opportunities will still exist for those who are well-informed, financially prepared, and adaptable.

In conclusion, the journey to 2026 for the housing market promises complexity and evolution. Understanding the interplay of supply constraints, persistent demand, and the critical impact of economic factors on affordability is key. By staying informed and adopting strategic approaches, participants can better navigate the challenges and capitalize on the opportunities that this dynamic environment will undoubtedly present.

")