Unlock Financial Growth: Master Compound Interest for 7% Annual Returns by 2026

Understanding Compound Interest: How to Grow Your Investments by 7% Annually Starting in 2026 (INSIDER KNOWLEDGE, FINANCIAL IMPACT)

In the vast landscape of personal finance, few concepts hold as much transformative power as compound interest growth. Often dubbed the ‘eighth wonder of the world’ by Albert Einstein, compound interest is the engine that can drive your investments to unprecedented heights, turning modest savings into substantial wealth over time. For those looking to significantly boost their financial standing and achieve a remarkable 7% annual return on investments by 2026, understanding and strategically harnessing the power of compound interest is not just an advantage – it’s a necessity.

This comprehensive guide dives deep into the mechanics of compound interest growth, offering insider knowledge and actionable strategies designed to maximize your financial impact. We’ll explore what compound interest truly means, how it works its magic, and, crucially, how you can leverage it to reach your specific financial goals, particularly targeting that ambitious 7% annual return in the coming years. Whether you’re a seasoned investor or just starting your financial journey, the principles outlined here will provide a robust framework for significant wealth accumulation.

What Exactly is Compound Interest and Why Does it Matter for Your Financial Future?

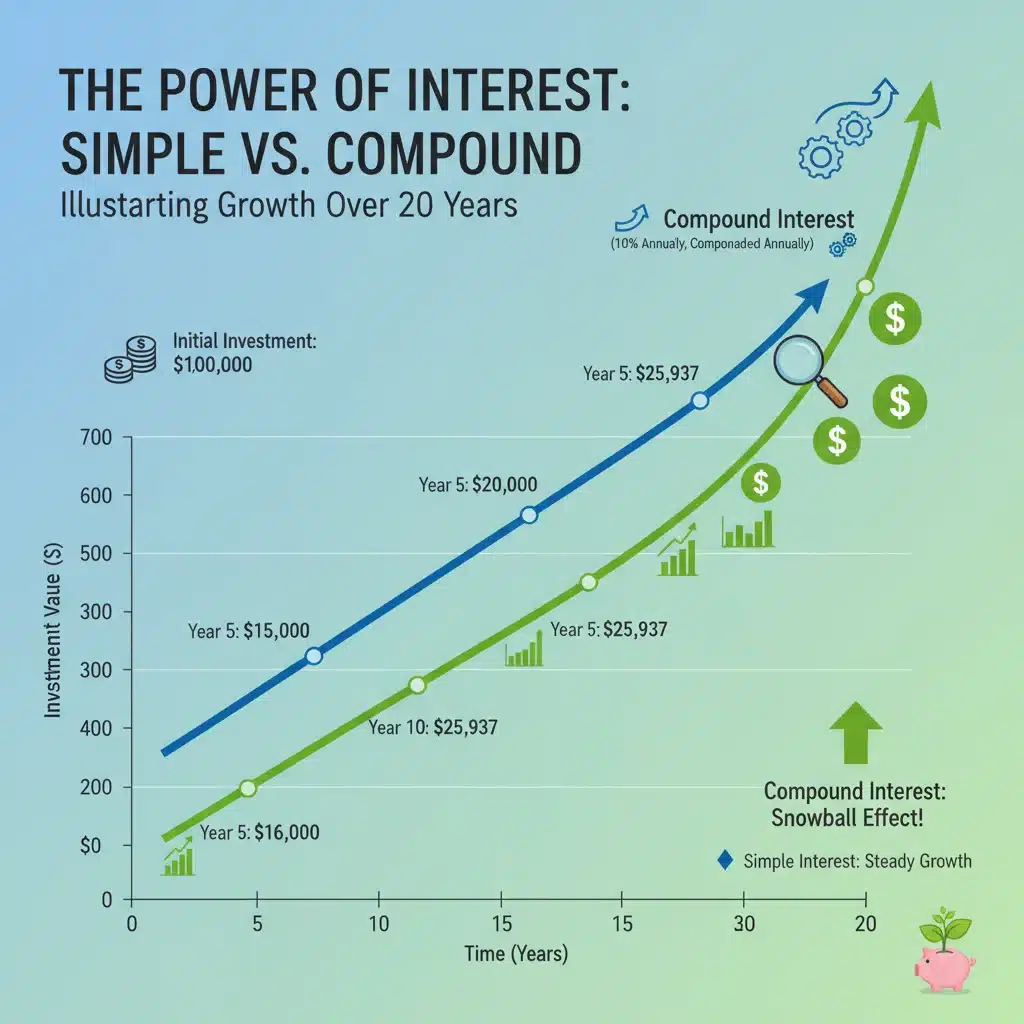

At its core, compound interest is interest calculated on the initial principal, which also includes all of the accumulated interest from previous periods on a deposit or loan. This concept is fundamentally different from simple interest, which is calculated only on the principal amount. The key differentiator, and where the ‘magic’ truly happens, is the reinvestment of earnings. When your interest earns interest, and that new, larger sum earns even more interest, you create an accelerating snowball effect that can dramatically increase your wealth.

Think of it this way: with simple interest, if you invest $1,000 at a 5% annual rate, you earn $50 each year. After 10 years, you’d have earned $500 in total interest, bringing your total to $1,500. With compound interest, however, that $50 earned in the first year is added to your principal, so in the second year, you’re earning interest on $1,050. This seemingly small difference compounds over time, leading to significantly larger returns. The longer your money is invested, the more powerful this compounding effect becomes. This is the cornerstone of effective compound interest growth.

For your financial future, understanding this distinction is paramount. It means that starting early, even with small amounts, can have a more profound impact than starting later with larger sums. It highlights the importance of not just saving, but also investing wisely and allowing your returns to compound over decades. This principle is the bedrock of long-term wealth building and financial independence.

The Formula Behind the Magic: How Compound Interest Works

While the concept of compound interest growth might seem abstract, its calculation is rooted in a straightforward formula. Knowing this formula can help you forecast your potential earnings and make informed investment decisions. The compound interest formula is:

A = P (1 + r/n)^(nt)

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

Let’s break this down with an example relevant to our goal of 7% annual returns. Suppose you invest $10,000 today with an annual interest rate of 7% (0.07) compounded annually (n=1) for 10 years (t=10). The calculation would be:

A = 10,000 (1 + 0.07/1)^(1*10)

A = 10,000 (1.07)^10

A ≈ 10,000 * 1.96715

A ≈ $19,671.51

After 10 years, your initial $10,000 would have nearly doubled to $19,671.51, almost entirely thanks to the power of compound interest growth. If this were simple interest, you would have only earned $700 per year for 10 years, totaling $7,000, bringing your sum to $17,000. The difference is significant!

Understanding each variable allows you to manipulate them to your advantage. For instance, increasing ‘P’ (your initial investment) or ‘t’ (the time horizon) will naturally lead to greater future value. Similarly, a higher ‘r’ (interest rate) or more frequent compounding (‘n’) can accelerate your wealth accumulation. This formula is your roadmap to predicting and achieving your financial milestones, especially when aiming for consistent compound interest growth.

Strategies for Achieving 7% Annual Returns by 2026

Targeting a 7% annual return is an ambitious yet achievable goal for many investors, especially when leveraging the power of compound interest growth. While past performance is never a guarantee of future results, a 7% average annual return is often considered a reasonable long-term expectation for a diversified portfolio, particularly one with exposure to equity markets. Here are several strategies and considerations to help you on your path to achieving this target by 2026:

1. Diversify Your Investment Portfolio

Diversification is key to managing risk and optimizing returns. Instead of putting all your eggs in one basket, spread your investments across various asset classes, industries, and geographies. A well-diversified portfolio might include:

- Stocks (Equities): Historically, stocks have provided the highest long-term returns. Focusing on a mix of large-cap, mid-cap, and small-cap companies, as well as growth and value stocks, can help mitigate individual company risk. Consider investing in exchange-traded funds (ETFs) or mutual funds that track broad market indices like the S&P 500, which have historically delivered average annual returns often exceeding 7% over long periods.

- Bonds: While typically offering lower returns than stocks, bonds provide stability and income, reducing overall portfolio volatility. A mix of government and corporate bonds can offer a balanced approach.

- Real Estate: Through REITs (Real Estate Investment Trusts) or direct investments, real estate can offer appreciation and income, acting as a hedge against inflation.

- Alternative Investments: Depending on your risk tolerance and knowledge, consider looking into commodities, private equity, or even crowdfunding, though these often come with higher risk.

The goal of diversification is to create a portfolio where different assets perform well under different market conditions, smoothing out your overall returns and enhancing your potential for consistent compound interest growth.

2. Maximize Contributions and Reinvest Earnings

The more you invest, the more you have available to compound. Make regular, consistent contributions to your investment accounts. Automate these contributions if possible, making saving and investing a habit rather than an afterthought. Furthermore, ensure that any dividends or interest earned from your investments are automatically reinvested. This is crucial for maximizing the effect of compound interest growth, as it means your earnings start earning their own returns immediately.

3. Minimize Fees and Taxes

High fees and taxes can significantly erode your returns, effectively slowing down your compound interest growth. Be mindful of expense ratios on mutual funds and ETFs, trading commissions, and advisory fees. Opt for low-cost index funds or ETFs where possible. Similarly, utilize tax-advantaged accounts like 401(k)s, IRAs, and HSAs. These accounts allow your investments to grow tax-deferred or tax-free, meaning more of your returns stay invested and continue to compound, leading to a much larger sum over time.

4. Understand and Manage Risk

Achieving a 7% annual return typically requires taking on some level of risk, as lower-risk investments like savings accounts or CDs rarely offer such returns. However, managing this risk is paramount. Understand your personal risk tolerance and align your investment choices accordingly. Don’t chase excessively high returns with overly speculative investments. Instead, focus on a balanced approach that aligns with your long-term goals and comfort level. Regular rebalancing of your portfolio can also help maintain your desired risk profile.

5. Leverage Time: The Greatest Ally of Compound Interest

As the compound interest formula clearly shows, time (t) is an exponential factor. The longer your money has to grow, the more pronounced the compounding effect becomes. While our target is 2026, thinking beyond that and committing to a long-term investment horizon will greatly enhance your overall wealth. Even small amounts invested early can outperform larger amounts invested later, purely due to the extra time for compound interest growth to work its magic. Start now, stay consistent, and let time be your most powerful financial tool.

Insider Knowledge: Advanced Tips for Supercharging Your Returns

Beyond the fundamental strategies, there are several advanced tips that can further accelerate your compound interest growth and help you hit that 7% annual return target by 2026. These insights often come from seasoned investors and financial experts who understand the nuances of market dynamics and strategic planning.

1. Dollar-Cost Averaging (DCA)

Dollar-cost averaging is an investment strategy in which you invest a fixed amount of money at regular intervals, regardless of the asset’s price. This approach helps reduce the impact of volatility. When prices are high, your fixed investment buys fewer shares; when prices are low, it buys more shares. Over time, this strategy can result in a lower average cost per share than if you tried to time the market. DCA is particularly effective for consistent compound interest growth because it encourages disciplined, regular investing, ensuring your money is always in the market and compounding.

2. Understanding the Impact of Inflation

While a 7% nominal return sounds great, it’s crucial to consider inflation. Inflation erodes the purchasing power of your money over time. If inflation is 3% and your investment earns 7%, your real (inflation-adjusted) return is closer to 4%. When setting your 7% target, it’s wise to consider whether this is a nominal or real return goal. For substantial compound interest growth in real terms, your investments must consistently outpace inflation. This often means leaning into growth-oriented assets like equities rather than solely relying on fixed-income investments.

3. Rebalancing Your Portfolio Regularly

Over time, different asset classes will perform differently, causing your portfolio’s allocation to drift from its original target. Rebalancing involves selling off assets that have performed well (and now represent a larger portion of your portfolio) and buying more of those that have underperformed (and now represent a smaller portion). This strategy helps you:

- Maintain your desired risk level.

- Systematically buy low and sell high.

- Ensure your portfolio remains aligned with your long-term compound interest growth objectives.

Regular rebalancing, typically once or twice a year, is a disciplined way to manage your portfolio actively without succumbing to emotional trading.

4. Consider Tax-Loss Harvesting

For investments held in taxable accounts, tax-loss harvesting can be a powerful strategy to reduce your tax burden, thereby allowing more capital to remain invested and compound. This involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. While it doesn’t directly increase your investment returns, it reduces the amount of taxes you pay, effectively increasing your net compound interest growth. Always consult with a tax professional before implementing tax-loss harvesting strategies.

5. Continuous Learning and Adaptation

The financial markets are dynamic. Economic conditions, geopolitical events, and technological advancements can all impact investment performance. Staying informed, continuously learning about new investment opportunities, and adapting your strategy as needed are crucial for sustained compound interest growth. This doesn’t mean constantly tinkering with your portfolio, but rather understanding the broader financial environment and making informed adjustments when necessary. Reading financial news, following reputable analysts, and understanding economic indicators can provide valuable insights.

The Financial Impact: Visualizing Your Compound Interest Growth Towards 2026 and Beyond

To truly appreciate the financial impact of achieving a 7% annual return through compound interest growth, let’s visualize some scenarios. These examples underscore why starting early and staying invested are non-negotiable for serious wealth builders.

Scenario 1: Early Starter

Imagine a 25-year-old who invests $500 per month and achieves a 7% annual return. By age 65 (40 years), they would have contributed $240,000. However, thanks to compound interest growth, their investment would be worth approximately $1,280,000. The interest earned ($1,040,000) far surpasses the principal contributed.

Scenario 2: Mid-Career Investor

Consider a 35-year-old who starts investing $700 per month at a 7% annual return. By age 65 (30 years), they would have contributed $252,000. Their investment would grow to roughly $850,000. While still significant, the total is less than the early starter, despite a higher monthly contribution, illustrating the power of time in compound interest growth.

Scenario 3: Late Starter

A 45-year-old starting with $1,000 per month, aiming for a 7% annual return until age 65 (20 years), would contribute $240,000. Their investment would reach approximately $490,000. Notice how the total contributed is similar to the early starter, but the final value is significantly lower due to less time for compounding. This emphasizes that while it’s never too late to start, the impact of time on compound interest growth is exponential.

These scenarios highlight a critical lesson: the most significant factor in maximizing compound interest growth is the duration of your investment. Every year your money is invested and compounding at 7% makes a substantial difference. By setting your sights on 2026, you’re not just aiming for a short-term gain; you’re building momentum for decades of financial prosperity.

Tools and Resources to Aid Your Compound Interest Journey

Navigating the world of investments and maximizing compound interest growth doesn’t have to be a solitary journey. Numerous tools and resources are available to help you plan, track, and optimize your financial strategy:

1. Compound Interest Calculators

These online tools allow you to input different variables (principal, interest rate, compounding frequency, time) to visualize potential investment growth. They are excellent for setting realistic goals and understanding the impact of various investment decisions on your compound interest growth.

2. Robo-Advisors

Platforms like Betterment, Wealthfront, and Fidelity Go offer automated investment management at a lower cost than traditional financial advisors. They build diversified portfolios based on your risk tolerance and goals, often rebalancing automatically, which is ideal for consistent compound interest growth without active management on your part.

3. Investment Tracking Apps

Apps such as Personal Capital, Mint, or Quicken allow you to aggregate all your financial accounts in one place, track your net worth, analyze your spending, and monitor your investment performance. This holistic view is crucial for staying on top of your financial health and ensuring your investments are on track for their 7% annual return target.

4. Financial Education Resources

Websites like Investopedia, NerdWallet, and reputable financial news outlets (e.g., The Wall Street Journal, Bloomberg) offer a wealth of articles, tutorials, and market insights. Continuous learning is a cornerstone of intelligent investing and maximizing compound interest growth.

5. Professional Financial Advisors

For complex financial situations or if you prefer personalized guidance, a certified financial planner (CFP) can provide tailored advice, help you develop a comprehensive financial plan, and assist in selecting appropriate investments to achieve your compound interest growth goals. Always look for fee-only fiduciaries who are legally obligated to act in your best interest.

Common Pitfalls to Avoid on Your Path to 7% Returns

While the path to significant compound interest growth and 7% annual returns is clear, it’s also fraught with potential pitfalls. Being aware of these common mistakes can help you navigate your investment journey more effectively:

1. Emotional Investing

Reacting to market fluctuations with fear or greed is one of the biggest destroyers of wealth. Selling during market downturns locks in losses, preventing your investments from recovering and compounding when the market rebounds. Conversely, chasing hot stocks or trends often leads to buying high and selling low. Stick to your long-term investment plan and avoid making impulsive decisions based on market noise. Discipline is paramount for consistent compound interest growth.

2. Lack of Diversification

As mentioned earlier, putting all your capital into a single asset or a few assets exposes you to immense risk. A sudden downturn in that specific investment can wipe out years of compound interest growth. Ensure your portfolio is adequately diversified across different asset classes, sectors, and geographies to cushion against unexpected shocks.

3. Excessive Fees and Costs

High expense ratios on funds, frequent trading commissions, and exorbitant advisory fees can eat into your returns significantly. Over decades, even a 1% difference in fees can amount to hundreds of thousands of dollars in lost compound interest growth. Be diligent about understanding all costs associated with your investments.

4. Ignoring Inflation

Failing to account for inflation can give you a false sense of security regarding your returns. A 7% nominal return might only be a 4% real return if inflation is 3%. Ensure your investment strategy aims for returns that comfortably outpace inflation to achieve true wealth accumulation through compound interest growth.

5. Not Reinvesting Dividends

Many investors overlook the power of reinvesting dividends. When companies pay out dividends, if you don’t reinvest them, you’re missing out on a significant opportunity for further compound interest growth. Automatically reinvesting dividends ensures that these earnings immediately start working for you, purchasing more shares and accelerating your compounding snowball.

6. Procrastination

The biggest enemy of compound interest growth is procrastination. The earlier you start, the more time your money has to compound, and the less you need to save each month to reach your goals. Delaying even by a few years can drastically reduce your potential future wealth. The best time to start investing was yesterday; the second best time is today.

Conclusion: Your Path to Accelerated Compound Interest Growth by 2026

The journey to achieving 7% annual returns on your investments by 2026, powered by compound interest growth, is an exciting and achievable one. It requires a clear understanding of financial principles, disciplined execution, and a long-term perspective. By embracing diversification, maximizing contributions, minimizing costs, and leveraging the invaluable gift of time, you can set a robust foundation for significant wealth accumulation.

Remember that compound interest is not a get-rich-quick scheme; it’s a patient, persistent strategy that rewards consistency and foresight. The insider knowledge and practical steps outlined in this guide are designed to equip you with the tools and confidence to navigate the investment landscape effectively. Start today, stay informed, and watch as the incredible power of compound interest growth transforms your financial future, not just by 2026, but for decades to come.

Your financial independence is within reach. By mastering compound interest, you’re not just investing money; you’re investing in a more secure and prosperous future for yourself and your loved ones. Take control of your financial destiny, harness the power of compounding, and embark on a journey of continuous growth.

Contributions for 2026: A Step-by-Step Guide to Reaching the $23,000 Limit")