Mastering 2026 AMT: Avoid Unexpected Tax Liabilities

The landscape of taxation is ever-evolving, and as we approach 2026, one particular aspect that demands meticulous attention is the Alternative Minimum Tax (AMT). For many high-income earners and those with specific types of deductions, the AMT can emerge as an unexpected and significant tax liability. It’s not merely an additional tax; rather, it’s a parallel tax system designed to ensure that certain taxpayers, who benefit from various tax preferences, pay at least a minimum amount of tax. Understanding and proactively navigating the 2026 AMT avoidance strategies is not just prudent; it’s essential for sound financial health.

Historically, the AMT was introduced in 1969 after 155 high-income households managed to legally avoid paying any federal income tax. Over the decades, it has undergone numerous reforms, but its fundamental purpose remains: to prevent taxpayers from using certain deductions, exclusions, and credits to reduce their regular taxable income below a specific threshold. While the Tax Cuts and Jobs Act (TCJA) of 2017 significantly increased the AMT exemption amounts and phase-out thresholds, reducing the number of taxpayers subject to it, these provisions are set to expire at the end of 2025. This means that for the 2026 tax year, the AMT could potentially impact a much broader range of individuals and families, making proactive planning for 2026 AMT avoidance more critical than ever.

The expiration of the TCJA provisions means that the AMT exemption amounts will revert to their pre-TCJA levels (adjusted for inflation), and the phase-out thresholds will also be significantly lower. This shift could pull many taxpayers who previously were not subject to AMT back into its purview. Furthermore, the types of deductions and income items that trigger AMT, such as state and local tax (SALT) deductions, certain investment income, and incentive stock options (ISOs), will once again play a more prominent role. Therefore, it’s not enough to simply prepare your taxes; you need to understand the nuances of the AMT and how your specific financial activities might interact with its complex rules to effectively implement 2026 AMT avoidance strategies.

This comprehensive guide aims to shed light on the intricacies of the 2026 AMT and, more importantly, equip you with three insider tips to proactively avoid unexpected tax liabilities. By understanding the triggers, leveraging strategic planning, and seeking expert advice, you can navigate the complexities of the 2026 tax season with confidence and ensure your financial future remains secure. Our goal is to empower you with the knowledge needed for effective 2026 AMT avoidance, transforming potential tax burdens into opportunities for optimized financial outcomes.

Understanding the Alternative Minimum Tax (AMT) for 2026

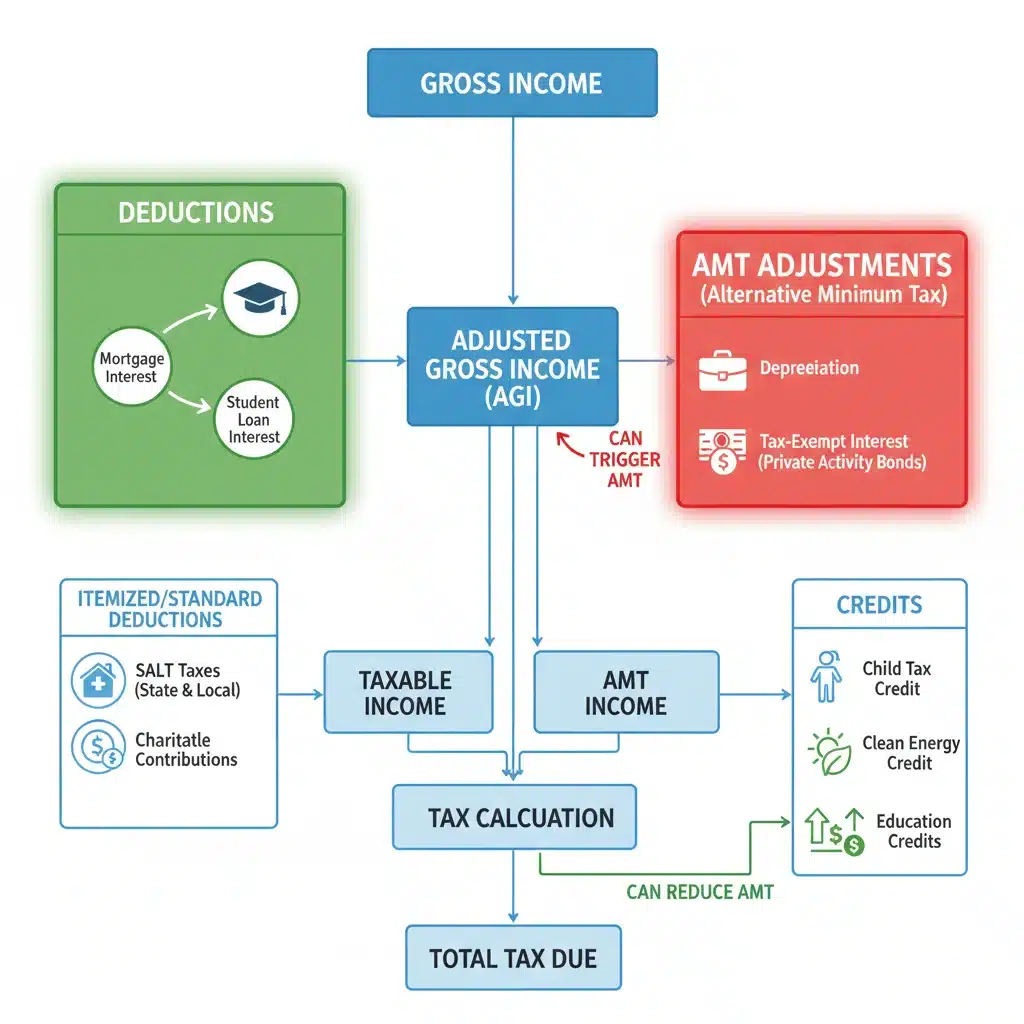

Before diving into avoidance strategies, it’s crucial to grasp what the AMT is and why it’s poised to become a more significant factor in 2026. The AMT functions as a separate tax calculation, running parallel to the regular income tax system. Taxpayers must calculate their tax liability under both systems and pay the higher of the two. The underlying principle is to ensure that individuals and corporations with substantial income, who might otherwise significantly reduce their tax burden through various deductions and credits, still pay a baseline amount of tax.

The Mechanics of AMT Calculation

The AMT calculation begins with your regular taxable income. To this, certain adjustments and preference items are added back. These typically include:

- State and Local Taxes (SALT) Deductions: Under the regular tax system, you can deduct up to $10,000 in state and local taxes. For AMT purposes, this deduction is generally disallowed, meaning it’s added back to your income. This is a significant factor for residents in high-tax states.

- Incentive Stock Options (ISOs): When you exercise ISOs, the difference between the fair market value of the stock and the exercise price is treated as income for AMT purposes, even if you don’t sell the stock immediately and realize a gain for regular tax purposes. This can create a significant phantom income problem.

- Miscellaneous Itemized Deductions: Before TCJA, these were disallowed for AMT. With the expiration of TCJA, these may become relevant again for AMT purposes.

- Depreciation: Certain accelerated depreciation methods allowed for regular tax purposes are adjusted for AMT, requiring a slower depreciation schedule for AMT calculations.

- Tax-Exempt Interest from Private Activity Bonds: While generally tax-exempt for regular income tax, interest from certain private activity bonds is included in AMT income.

After these adjustments, you arrive at your Alternative Minimum Taxable Income (AMTI). From this, you subtract an AMT exemption amount. The exemption amount is designed to protect lower and middle-income taxpayers from the AMT. However, this exemption is subject to a phase-out for higher-income taxpayers. As your AMTI exceeds a certain threshold, the exemption amount begins to decrease until it is completely phased out. This is where the 2026 changes become critical; the lower exemption amounts and phase-out thresholds will expose more taxpayers to the AMT.

Once the exemption is applied, the remaining amount is taxed at AMT rates, which are typically 26% and 28%. The final AMT liability is then compared to your regular tax liability, and you pay the higher of the two. This intricate process underscores why proactive 2026 AMT avoidance is so vital.

Why 2026 is Different: The TCJA Sunset

The Tax Cuts and Jobs Act of 2017 brought substantial changes to the AMT, primarily by increasing the exemption amounts and the income thresholds at which those exemptions begin to phase out. This significantly reduced the number of taxpayers subject to AMT. For instance, in 2017, before TCJA, millions of households paid AMT. After TCJA, that number dropped dramatically. However, these beneficial provisions are temporary and are set to expire on December 31, 2025.

When the TCJA provisions sunset, the AMT exemption amounts and phase-out thresholds will revert to their pre-TCJA levels, adjusted for inflation. This reversion means:

- Lower Exemption Amounts: A smaller portion of your income will be exempt from AMT.

- Lower Phase-Out Thresholds: The income level at which your AMT exemption begins to disappear will be significantly lower, impacting a broader range of high-income earners.

- Reintroduction of Certain Deductions as AMT Triggers: While the TCJA eliminated the deduction for miscellaneous itemized deductions and limited the SALT deduction, their treatment under AMT will revert, potentially making them more significant factors in triggering AMT.

This impending change makes understanding 2026 AMT avoidance strategies more urgent than ever. Many taxpayers who haven’t worried about AMT in recent years might find themselves unexpectedly subject to it, leading to higher tax bills than anticipated. Therefore, it’s not enough to rely on past tax experiences; a forward-looking approach to tax planning is essential for 2026.

Tip 1: Strategic Management of Incentive Stock Options (ISOs) and Capital Gains

One of the most common and often surprising triggers for the AMT is the exercise of Incentive Stock Options (ISOs). Unlike Non-Qualified Stock Options (NSOs), ISOs offer favorable tax treatment for regular income tax purposes: there’s no taxable income at exercise, and if held long enough, any gain upon sale is taxed at lower long-term capital gains rates. However, for AMT purposes, the spread between the exercise price and the fair market value of the stock on the exercise date is considered an AMT adjustment, increasing your AMTI. This can lead to a substantial AMT liability even if you haven’t sold the stock and thus haven’t realized any cash to pay the tax. This scenario is often referred to as the ‘phantom income’ problem.

Understanding ISOs and AMT Triggers

When you exercise ISOs, the difference between what you paid for the shares (exercise price) and what they were worth on the day you exercised them (fair market value) is added back to your income for AMT calculations. If you hold onto the shares, this ‘paper gain’ can still trigger AMT. If you sell the shares in the same year you exercise them, it’s a ‘disqualifying disposition,’ and the income is typically treated as ordinary income for regular tax, often lessening the AMT impact, but potentially increasing regular tax. The goal for 2026 AMT avoidance in this context is to carefully time your exercises and sales.

Proactive Strategies for ISOs

- Timing Exercises and Sales: This is perhaps the most critical strategy. Instead of exercising all your ISOs at once, consider a staggered approach. Exercise a portion each year to keep your AMTI below the AMT exemption or phase-out thresholds. If you plan to sell the stock, consider a ‘same-day sale’ or a ‘disqualifying disposition’ strategy if it helps mitigate AMT by altering the income recognition for regular tax purposes. Consult with a tax advisor to model various scenarios and determine the optimal timing for your specific situation.

- Understanding the AMT Credit: If you pay AMT due to ISOs, you generally generate an AMT credit. This credit can be used in future years to offset regular tax liability, but only to the extent that your regular tax exceeds your AMT in those future years. This credit can be a valuable asset, but its utilization can be complex and may take several years. Incorporating the potential for this credit into your long-term financial planning is crucial for effective 2026 AMT avoidance.

- Early Exercise and Section 83(b) Election: For some early-stage companies, you might have the option to exercise ISOs before they vest. If you do this and the stock’s fair market value is close to the exercise price, you can make a Section 83(b) election. This election allows you to recognize the spread as income (for regular and AMT purposes) at the time of exercise, even if the shares haven’t vested. If the value is low, this can result in minimal or no immediate tax, and future appreciation is then taxed as long-term capital gains, potentially avoiding a large AMT hit later. This is a highly specialized strategy and requires careful consideration of the company’s growth prospects and your liquidity.

- Diversification and Cash Flow Planning: If you anticipate a significant AMT liability from ISOs, ensure you have sufficient cash flow to cover the tax. This might involve selling a portion of your exercised shares, even if it’s not ideal from an investment perspective, or having other liquid assets readily available. Diversifying your investments can also help reduce reliance on a single equity source, mitigating large, sudden AMT triggers.

Managing Capital Gains and Losses

While capital gains themselves aren’t an AMT preference item, they can significantly increase your overall income, pushing you into higher tax brackets where AMT is more likely to apply, especially with the reduced exemption amounts in 2026. Strategic management of capital gains and losses is therefore an indirect but important component of 2026 AMT avoidance.

- Tax-Loss Harvesting: Regularly review your investment portfolio for opportunities to realize capital losses. These losses can offset capital gains and up to $3,000 of ordinary income annually. This strategy can reduce your overall taxable income, potentially keeping you below AMT thresholds or reducing your AMTI.

- Timing Sales: If you have significant appreciated assets, consider spreading sales over multiple tax years to avoid a large income spike in any single year. This can help manage your AMTI and keep you out of the AMT’s reach.

- Qualified Dividends and Long-Term Capital Gains: For AMT purposes, qualified dividends and long-term capital gains are generally taxed at the same preferential rates as for regular tax. However, the inclusion of these gains in your AMTI can still push you past the AMT exemption phase-out thresholds, indirectly increasing your AMT exposure.

Tip 2: Optimize Deductions and Credits with AMT in Mind

The core of the AMT lies in disallowing or adjusting certain deductions and credits that are perfectly legitimate under the regular tax system. With the TCJA provisions expiring, many of these will revert to their pre-2018 treatment, making it paramount to understand which deductions are ‘AMT-friendly’ and which are not. Optimizing your deductions and credits with 2026 AMT avoidance as a primary goal can significantly impact your final tax liability.

Key Deductions and Their AMT Treatment

As mentioned, the expiration of TCJA means that certain deductions will once again be added back for AMT calculations, increasing your AMTI. Here’s a closer look:

- State and Local Taxes (SALT) Deduction: This is arguably the most impactful change for many taxpayers. For regular tax purposes, the SALT deduction is capped at $10,000. For AMT, this deduction is completely disallowed. If you pay significant state and local income or property taxes, this amount will be added back to your income for AMT purposes, dramatically increasing your AMTI. Strategies to mitigate this include:

- Accelerating or Deferring Payments: If possible, strategically pay your state and local taxes in a year where you anticipate not being subject to AMT, or where the AMT impact will be less severe.

- Considering a Pass-Through Entity (PTE) Tax Election: Some states have enacted PTE taxes that allow pass-through entities (like S corporations or partnerships) to pay state income tax at the entity level. This can effectively bypass the $10,000 SALT cap for federal income tax purposes and, importantly, might also be deductible for AMT purposes, depending on specific state and federal guidance. This is a complex area and requires professional advice for 2026 AMT avoidance.

- Home Equity Interest: Before TCJA, interest on home equity loans was deductible for regular tax if the loan was used to buy, build, or substantially improve your home. For AMT, this deduction was often disallowed if the loan proceeds weren’t used to acquire or improve your main home. With the sunset, this could become a factor again.

- Miscellaneous Itemized Deductions Subject to the 2% AGI Limit: These deductions (e.g., unreimbursed employee expenses, investment expenses, tax preparation fees) were eliminated by TCJA. Upon sunset, they might return for regular tax purposes but are generally disallowed for AMT, again increasing AMTI.

- Medical Expense Deductions: While deductible for regular tax above a certain Adjusted Gross Income (AGI) threshold (e.g., 7.5% or 10%), for AMT, the threshold was historically higher (10% of AGI). This difference could lead to more medical expenses being disallowed for AMT.

AMT-Friendly Deductions and Credits

Not all deductions and credits are treated unfavorably by the AMT. Some can still reduce your AMTI or offset your AMT liability. Focusing on these can be a powerful 2026 AMT avoidance strategy:

- Mortgage Interest on Your Primary Residence: Interest on loans used to acquire or improve your primary residence (and one other home) remains deductible for AMT purposes, generally up to the same limits as regular tax.

- Charitable Contributions: Qualified cash and non-cash charitable contributions are generally deductible for AMT purposes, making them a powerful tool for reducing both regular and AMT liability. Consider ‘bunching’ your charitable contributions into a single year to exceed the standard deduction and maximize the tax benefit, especially if you anticipate being in an AMT position.

- Certain Tax Credits: While many non-refundable personal credits are disallowed for AMT, some credits, like the Child Tax Credit or certain education credits, can reduce your regular tax liability before the AMT calculation, potentially keeping your regular tax below your AMT. Foreign tax credits can also generally offset AMT.

- Health Savings Account (HSA) Contributions: Contributions to an HSA are deductible for both regular tax and AMT purposes, offering a dual tax advantage. This makes HSAs an excellent vehicle for tax-advantaged savings and a useful tool for 2026 AMT avoidance.

The key here is to meticulously review your itemized deductions and understand their specific treatment under both regular tax and AMT rules. A tax professional can help you identify which deductions will be most beneficial and how to structure your financial activities to maximize AMT-friendly deductions while minimizing those that trigger AMT adjustments.

Tip 3: Proactive Year-End Planning and Professional Guidance

Effective 2026 AMT avoidance isn’t a one-time event; it’s an ongoing process that culminates in strategic year-end tax planning. Given the complexities and the impending changes in 2026, relying on guesswork or last-minute adjustments is a recipe for unexpected tax liabilities. Proactive planning, ideally starting well before year-end, and seeking expert advice are indispensable.

Year-End Tax Planning for AMT

As the year draws to a close, several actions can be taken to influence your AMT position:

- Conduct a Mid-Year Tax Projection: Don’t wait until December. By mid-year (or even earlier), work with a tax professional to project your income, deductions, and potential AMT liability for the upcoming 2026 tax year. This projection should consider the sunsetting of TCJA provisions. This early insight allows you to take corrective actions while there’s still time.

- Income Acceleration/Deferral: Depending on your projected AMT status, you might consider accelerating income into a year where you anticipate lower AMT exposure or deferring income into a year where you expect to be below the AMT threshold or have sufficient AMT credits to offset it. For instance, if you expect to be subject to AMT in 2026, but not in 2025, accelerating bonuses or exercising stock options in 2025 could be beneficial. Conversely, deferring income into 2026 if you expect to have a lower overall tax burden (or to use AMT credits) could be advantageous.

- Deduction Planning: As discussed in Tip 2, strategically timing your deductible expenses is crucial. For example, if you are on the cusp of AMT, consider accelerating deductible expenses (like charitable contributions or medical expenses if they exceed the AGI threshold) into a year where they will provide the most benefit against regular tax, or conversely, deferring them if they will be disallowed for AMT and provide no benefit.

- Review Your Withholding and Estimated Payments: If you anticipate an AMT liability, ensure your withholding or estimated tax payments are sufficient to cover both your regular tax and potential AMT. Underpaying can lead to penalties.

- Consider Tax-Advantaged Investments: Explore investments that are less likely to trigger AMT or that offer AMT-friendly deductions. For example, municipal bonds, while generally tax-exempt for regular income tax, can sometimes generate interest that is taxable for AMT if they are ‘private activity bonds.’ Understanding the specific nature of your tax-exempt investments is crucial.

The Indispensable Role of Professional Guidance

The complexity of the AMT, especially with the impending changes in 2026, makes professional tax advice not just helpful but often essential. A qualified tax advisor can:

- Perform Detailed Projections: They can run sophisticated tax projections that account for all your income sources, deductions, and potential AMT triggers, giving you a clear picture of your 2026 tax liability.

- Identify Specific Triggers: A professional can pinpoint which of your financial activities are most likely to trigger AMT and help you devise strategies to mitigate their impact. This is particularly true for complex situations involving ISOs, significant capital gains, or unique investment portfolios.

- Navigate Legislative Changes: Tax laws are dynamic. A tax professional stays abreast of the latest legislative developments, including any potential changes or extensions to the TCJA provisions, ensuring your planning is based on the most current information.

- Develop Personalized Strategies: Generic advice rarely fits unique financial situations. A tax advisor can develop a customized 2026 AMT avoidance plan tailored to your specific income, assets, and financial goals. This might involve recommending specific investment strategies, timing of transactions, or charitable giving approaches.

- Ensure Compliance: Beyond avoidance, a professional ensures that your tax planning and filing are fully compliant with all IRS regulations, minimizing the risk of audits or penalties.

Engaging a tax professional early in the year, particularly for the 2026 tax year, will afford you the maximum opportunity to implement effective 2026 AMT avoidance strategies. Don’t wait until tax season to discover you have an unexpected AMT bill; proactive engagement is your best defense.

The Future of AMT Beyond 2026

While our focus is primarily on 2026 AMT avoidance, it’s worth noting that the tax landscape is always subject to change. The sunsetting of the TCJA provisions is a significant event, but future legislative actions could once again alter the AMT. Policymakers may choose to extend some or all of the TCJA provisions, modify the AMT further, or even repeal it entirely. Keeping an eye on political and economic developments is part of a holistic financial planning strategy.

For now, the prudent approach is to plan based on current law and the scheduled expiration of the TCJA provisions. This means operating under the assumption that the AMT will revert to its more expansive form in 2026. Any future changes would then be a bonus, but planning for the worst-case scenario (from a tax perspective) ensures you are prepared.

It’s also important to remember that the AMT is not inherently ‘bad.’ It serves a purpose in the tax system. However, for individual taxpayers, it can be a complex and sometimes unfair burden, especially when it taxes ‘phantom income’ or disallows deductions that are otherwise beneficial. The goal of 2026 AMT avoidance is not to evade taxes but to legally and strategically minimize your tax liability within the confines of the law, ensuring your financial resources are allocated efficiently.

Conclusion: Empowering Your 2026 AMT Avoidance Strategy

The 2026 tax year presents a unique challenge for many taxpayers due to the scheduled expiration of the Tax Cuts and Jobs Act provisions and the subsequent resurgence of the Alternative Minimum Tax. Understanding the mechanics of the AMT, identifying common triggers like ISOs and certain deductions, and implementing proactive planning strategies are paramount for effective 2026 AMT avoidance.

By strategically managing your Incentive Stock Options and capital gains, optimizing your deductions and credits with AMT implications in mind, and engaging in proactive year-end planning with the guidance of a qualified tax professional, you can significantly mitigate the risk of unexpected tax liabilities. The tips provided in this guide – focusing on ISO and capital gains management, optimizing deductions, and proactive planning with professional help – form a robust framework for navigating the complexities of the 2026 AMT.

Remember, foresight and timely action are your greatest assets in tax planning. Don’t let the 2026 AMT catch you by surprise. Start your planning today, consult with experts, and empower yourself with the knowledge to ensure your financial future remains secure and optimized. The path to successful 2026 AMT avoidance begins with informed decisions and strategic execution.