Mastering 2026 Retirement Contributions: Your Guide to Tax-Advantaged Savings

Retirement planning is a journey, not a destination, and each year brings new opportunities and, often, new guidelines. As we look ahead to 2026, understanding the nuances of 2026 Retirement Contributions is paramount for anyone serious about securing their financial future. The decisions you make now regarding your retirement accounts can have a profound impact on your long-term wealth accumulation, offering significant tax advantages that can accelerate your savings growth. This comprehensive guide will delve into the essential aspects of optimizing your 2026 retirement contributions, covering everything from understanding various account types to strategizing for maximum benefit.

Navigating the world of retirement savings can feel daunting, with a myriad of acronyms and rules to decipher. However, by breaking down the key components of 2026 Retirement Contributions, you can empower yourself to make informed choices that align with your financial goals. Whether you’re a seasoned investor or just starting your retirement savings journey, this article aims to provide actionable insights and clarity on how to best utilize the tax-advantaged vehicles available to you in 2026.

The landscape of retirement planning is dynamic, influenced by economic factors, legislative changes, and personal circumstances. Staying informed about the latest contribution limits and rules for 2026 is crucial for maximizing your savings potential. This guide will serve as your go-to resource, ensuring you are well-equipped to make the most of your 2026 Retirement Contributions and pave the way for a comfortable and secure retirement.

Understanding the Core of 2026 Retirement Contributions

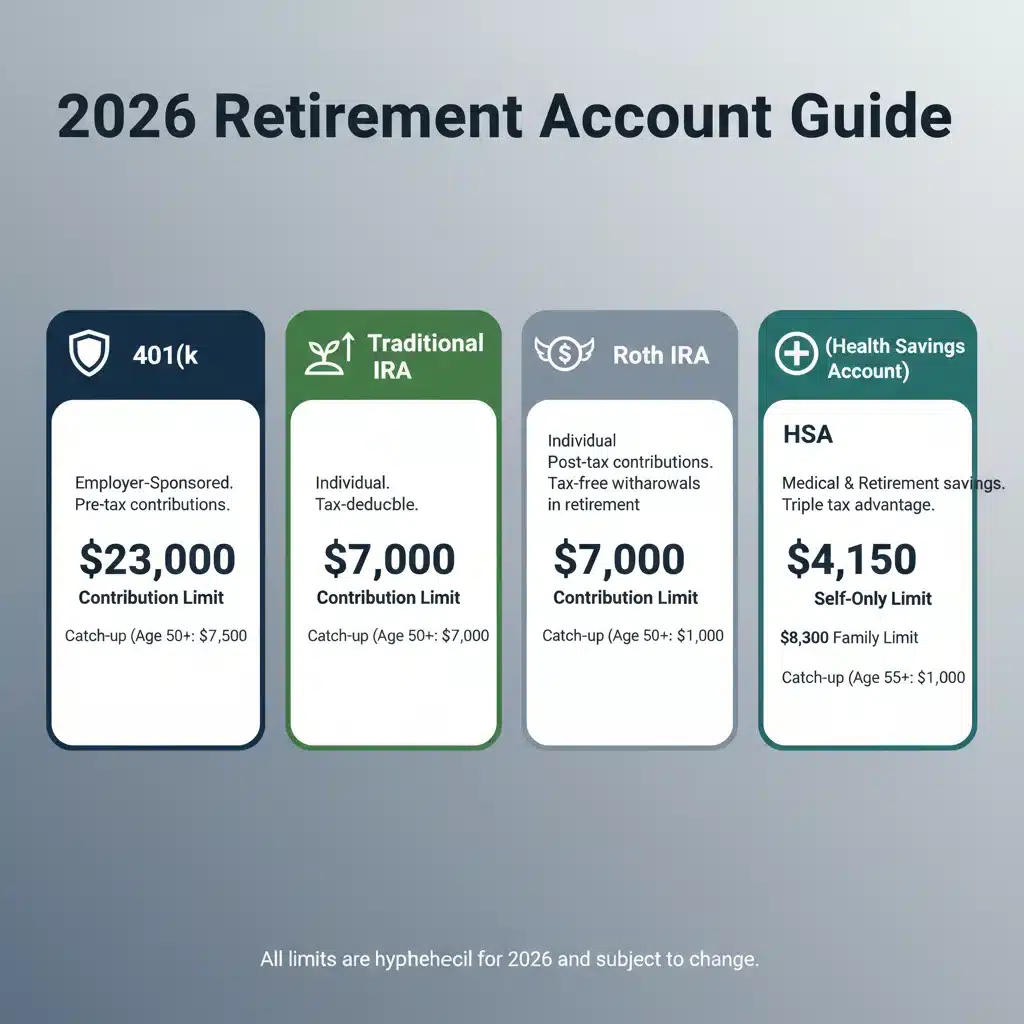

At the heart of effective retirement planning lies a clear understanding of the different types of retirement accounts and their unique features. Each account offers distinct tax advantages, and choosing the right combination can significantly impact your net savings. For 2026 Retirement Contributions, the primary vehicles you’ll encounter include 401(k)s, Traditional IRAs, Roth IRAs, and Health Savings Accounts (HSAs).

401(k) Plans: The Workplace Powerhouse

For many employees, the 401(k) is the cornerstone of their retirement strategy. These employer-sponsored plans allow you to contribute a portion of your pre-tax salary, reducing your taxable income in the present. The money grows tax-deferred, meaning you don’t pay taxes on investment gains until withdrawal in retirement. Many employers also offer matching contributions, which is essentially free money and a powerful incentive to maximize your 2026 Retirement Contributions to your 401(k).

- Pre-tax Contributions: Reduces current taxable income.

- Tax-Deferred Growth: Investment gains are not taxed until withdrawal.

- Employer Match: A significant boost to your savings.

- High Contribution Limits: Generally higher than IRAs, allowing for substantial savings.

While the exact 401(k) contribution limits for 2026 will be announced later, they typically see inflation-adjusted increases each year. It’s vital to stay updated on these limits to ensure you’re contributing the maximum allowed, especially if your employer offers a match. Failing to contribute enough to capture the full employer match is one of the most common retirement planning mistakes. Make it a priority to understand your plan’s specifics for 2026 Retirement Contributions.

Traditional IRAs: Personal Retirement Savings

Individual Retirement Arrangements (IRAs) offer a flexible way to save for retirement, particularly for those whose employers don’t offer a 401(k) or who wish to supplement their workplace plan. Traditional IRAs allow pre-tax contributions for many individuals, leading to a tax deduction in the year of contribution. Like 401(k)s, the investments grow tax-deferred until retirement. However, there are income limitations for deducting Traditional IRA contributions if you or your spouse are covered by a workplace retirement plan.

- Tax-Deductible Contributions: May lower your current tax bill.

- Tax-Deferred Growth: Taxes paid only upon withdrawal.

- Flexibility: Wide range of investment options.

- Income Limitations: Deductibility can be phased out based on income and workplace plan coverage.

Understanding the deductibility rules for Traditional IRA 2026 Retirement Contributions is key. If your income is too high to deduct contributions, you can still make non-deductible contributions, which can be part of a ‘backdoor Roth’ strategy, a topic we’ll touch upon later. Always consult with a financial advisor to determine the best approach for your specific situation.

Roth IRAs: Tax-Free Growth in Retirement

Roth IRAs are a favorite among many for their unique tax advantage: qualified withdrawals in retirement are entirely tax-free. This means that while your contributions are made with after-tax dollars (no upfront tax deduction), all your investment growth and withdrawals in retirement are free from federal income tax, provided certain conditions are met (e.g., account open for at least five years and you’re over 59½). This makes Roth IRAs incredibly attractive for those who anticipate being in a higher tax bracket in retirement or who want to diversify their tax exposure.

- Tax-Free Withdrawals: A major benefit in retirement.

- After-Tax Contributions: No upfront tax deduction.

- Income Limitations: Eligibility is phased out for higher earners.

- No Required Minimum Distributions (RMDs) for original owner: More control over your money.

The income limits for Roth IRA 2026 Retirement Contributions are a critical consideration. If your modified adjusted gross income (MAGI) exceeds these limits, you may not be able to contribute directly to a Roth IRA. However, the ‘backdoor Roth IRA’ strategy allows high-income earners to indirectly contribute to a Roth by making non-deductible Traditional IRA contributions and then converting them to a Roth. This strategy is perfectly legal but requires careful execution to avoid tax pitfalls.

Health Savings Accounts (HSAs): The Triple Tax Advantage

Often overlooked as a powerful retirement savings tool, Health Savings Accounts (HSAs) offer what is known as a ‘triple tax advantage.’ Contributions are tax-deductible, the money grows tax-free, and qualified withdrawals for medical expenses are also tax-free. To be eligible for an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP).

- Tax-Deductible Contributions: Lowers taxable income.

- Tax-Free Growth: Investments grow without tax.

- Tax-Free Withdrawals for Medical Expenses: Unmatched tax efficiency.

- Portability: You own the account, even if you change employers.

While primarily designed for healthcare expenses, the unique tax benefits of HSAs make them an excellent supplementary retirement vehicle. If you can afford to pay for current medical expenses out-of-pocket, you can let your HSA funds grow untouched for decades. In retirement, these funds can be used for any purpose, though withdrawals for non-medical expenses will be taxed as ordinary income after age 65 (like a Traditional IRA). For 2026 Retirement Contributions, maximizing your HSA contributions, if eligible, is a highly recommended strategy for long-term financial health and retirement security.

Projected 2026 Retirement Contributions Limits and Key Dates

While the official 2026 Retirement Contributions limits are typically announced by the IRS in late fall of the preceding year (e.g., late 2025 for 2026), we can anticipate general trends and potential increases based on inflation and economic indicators. It’s important to remember that these are projections, and the final numbers may vary. However, planning around these estimates can help you prepare.

Estimated Contribution Limits for 2026

The IRS usually adjusts contribution limits for various retirement plans annually based on cost-of-living adjustments. Here’s what we might expect for 2026:

- 401(k), 403(b), TSP, and 457(b) plans: The limit for employee contributions (elective deferrals) has consistently increased. For 2025, it was $23,000, and it’s reasonable to expect a slight increase for 2026, potentially reaching around $23,500 – $24,000.

- Catch-Up Contributions (Age 50 and Over) for 401(k)s: These allow older workers to contribute an additional amount. For 2025, this was $7,500. A similar or slightly higher amount is expected for 2026, possibly $7,500 – $8,000.

- Traditional and Roth IRAs: The limit for 2025 was $7,000. We could see this increase to $7,500 for 2026, or remain constant depending on inflation.

- Catch-Up Contributions (Age 50 and Over) for IRAs: This limit was $1,000 for 2025 and is statutory, meaning it does not typically change with inflation, so it is expected to remain $1,000 for 2026.

- Health Savings Accounts (HSAs): These limits are also adjusted annually. For 2025, the self-only coverage limit was $4,300, and family coverage was $8,550. Expect modest increases for 2026.

- HSA Catch-Up Contributions (Age 55 and Over): This remains a statutory $1,000 and is not expected to change for 2026.

These projected figures for 2026 Retirement Contributions are crucial for planning your annual savings strategy. Once the official limits are released, it’s important to review them and adjust your contributions accordingly. Setting up automatic contributions to hit these maximums early in the year can be a highly effective strategy, leveraging dollar-cost averaging and maximizing your time in the market.

Important Dates for 2026 Retirement Contributions

Beyond the limits, understanding key dates is also vital:

- Contribution Deadline for IRAs: Contributions for the 2026 tax year can typically be made up until the tax filing deadline of April 15, 2027 (or the next business day if April 15th falls on a weekend or holiday). This gives you extra time to fund your IRA for the previous year.

- 401(k) Contribution Deadline: Your 401(k) contributions for 2026 must be made by December 31, 2026, as they are deducted directly from your paychecks throughout the year.

- HSA Contribution Deadline: Similar to IRAs, HSA contributions for the 2026 tax year can typically be made up until the tax filing deadline of April 15, 2027.

Marking these dates on your calendar can help you stay organized and ensure you don’t miss out on maximizing your 2026 Retirement Contributions. Proactive planning is always better than reacting at the last minute.

Strategizing for Maximum 2026 Retirement Contributions

Simply knowing the limits isn’t enough; you need a strategy to effectively utilize these accounts. Maximizing your 2026 Retirement Contributions involves a thoughtful approach that considers your current financial situation, future goals, and risk tolerance. Here are some key strategies:

1. Prioritize Employer Match

This cannot be stressed enough: if your employer offers a 401(k) match, contribute at least enough to get the full match. It’s an immediate, guaranteed return on your investment, often 50% or 100%, which is hard to beat anywhere else. Missing out on an employer match is leaving free money on the table, directly hindering your 2026 Retirement Contributions growth.

2. Max Out Your 401(k) (or Other Workplace Plan)

After securing the employer match, if your budget allows, aim to contribute the maximum possible to your 401(k). The high contribution limits and tax-deferred growth make it an incredibly powerful tool for accumulating wealth. Consider increasing your contribution percentage each year, especially when you receive a raise, to gradually reach the maximum for your 2026 Retirement Contributions.

3. Contribute to an IRA (Traditional or Roth)

Once your workplace plan is maximized (or if you don’t have one), turn your attention to an IRA. The choice between a Traditional and Roth IRA depends on your current income, expected future income, and tax philosophy:

- Choose Roth if: You expect to be in a higher tax bracket in retirement than you are now, or if you want tax diversification and the flexibility of tax-free withdrawals. This is often a good choice for younger workers.

- Choose Traditional if: You are in a high tax bracket now and anticipate being in a lower one in retirement, or if you want the upfront tax deduction.

Don’t forget about the potential for a ‘backdoor Roth IRA’ if your income exceeds the direct Roth contribution limits. This strategy involves contributing non-deductible funds to a Traditional IRA and then converting them to a Roth. It’s a common and legal way for high-income earners to participate in Roth 2026 Retirement Contributions.

4. Leverage Your HSA for Long-Term Savings

If you’re eligible for an HSA, maximize your contributions. Treat it as an investment account, not just a spending account for medical expenses. Pay for current medical costs out-of-pocket if possible, allowing the HSA funds to grow tax-free. In retirement, it acts as a flexible fund for healthcare costs (tax-free) or general living expenses (taxable, like a Traditional IRA, after age 65). This makes it an incredibly versatile tool for your 2026 Retirement Contributions.

5. Utilize Catch-Up Contributions (If Applicable)

If you’re age 50 or older, take full advantage of catch-up contributions for your 401(k) and IRA. These additional amounts allow you to supercharge your savings in the years leading up to retirement, making up for any periods when you couldn’t contribute as much. These are critical components of maximizing your 2026 Retirement Contributions if you qualify.

6. Consider Spousal IRAs

If you’re married and one spouse earns little or no income, a spousal IRA allows the working spouse to contribute to an IRA on behalf of the non-working spouse. This effectively doubles your household’s IRA contribution potential for 2026 Retirement Contributions, providing two separate retirement accounts that can grow independently.

7. Automate Your Savings

Set up automatic contributions to your retirement accounts from each paycheck. This ‘set it and forget it’ approach ensures consistency and helps you stay on track to meet your 2026 Retirement Contributions goals without having to actively think about it every month. Even small, regular increases can make a huge difference over time due to the power of compounding.

Beyond Contributions: Investment Strategy and Rebalancing

While maximizing your 2026 Retirement Contributions is a critical first step, how you invest those contributions is equally important. A well-thought-out investment strategy within your retirement accounts can significantly enhance your long-term growth.

Asset Allocation and Diversification

Your asset allocation — the mix of stocks, bonds, and other investments — should align with your risk tolerance and time horizon. Younger investors with a longer time horizon typically can afford to take on more risk, leaning towards a higher percentage of equities. As you approach retirement, it’s generally advisable to shift towards a more conservative allocation to protect your accumulated capital. Diversification across different asset classes, industries, and geographies helps mitigate risk and smooth out returns.

Regular Rebalancing

Over time, market fluctuations can cause your asset allocation to drift from your target. Regular rebalancing — typically once a year — involves selling assets that have grown significantly and buying those that have underperformed, bringing your portfolio back to its desired allocation. This disciplined approach ensures you’re maintaining your intended risk level and can even provide a ‘buy low, sell high’ mechanism. Rebalancing your portfolio within your 2026 Retirement Contributions is a smart move.

Understanding Fees

Be mindful of the fees associated with your retirement accounts and investments. High fees, even seemingly small percentages, can eat into your returns significantly over decades. Look for low-cost index funds, exchange-traded funds (ETFs), or target-date funds within your 401(k) and IRA. Understanding the expense ratios of your chosen investments is a fundamental aspect of maximizing the net growth of your 2026 Retirement Contributions.

Tax-Efficient Investing

Consider where you hold different types of investments to optimize tax efficiency. For example, tax-inefficient assets (like actively managed funds with high turnover or REITs) might be better held in tax-advantaged accounts like 401(k)s or Traditional IRAs, where their gains aren’t taxed until withdrawal. Tax-efficient assets (like broad-market index funds) could be held in taxable accounts or Roth IRAs, where their growth is either lightly taxed or tax-free upon withdrawal. This strategic placement enhances the overall value of your 2026 Retirement Contributions.

Common Pitfalls to Avoid with 2026 Retirement Contributions

Even with the best intentions, some common mistakes can derail your retirement savings. Being aware of these can help you steer clear:

- Not Starting Early Enough: The power of compounding interest is immense. Delaying your 2026 Retirement Contributions means missing out on years of potential growth. Every year counts.

- Under-Contributing: Only contributing enough to get the employer match is a good start, but often not enough to fund a comfortable retirement. Aim to maximize your contributions across all available accounts.

- Ignoring Inflation: The cost of living will increase over time. Your retirement savings need to grow faster than inflation to maintain purchasing power.

- Taking Early Withdrawals: Withdrawing funds from retirement accounts before age 59½ usually incurs a 10% penalty in addition to ordinary income taxes. This significantly hinders your long-term growth and should be avoided unless absolutely necessary.

- Being Too Conservative: Especially for younger investors, holding too much in cash or low-growth investments can lead to underperformance. While avoiding excessive risk is wise, a balanced approach is key.

- Not Reviewing Your Plan Regularly: Life changes — income increases, family situations evolve, and retirement goals shift. Regularly review your 2026 Retirement Contributions strategy, at least annually, to ensure it still aligns with your circumstances.

- Failing to Understand Tax Implications: Different accounts have different tax treatments. Misunderstanding these can lead to unexpected tax bills in retirement or missed opportunities for tax savings now.

Seeking Professional Guidance for Your 2026 Retirement Contributions

While this guide provides a comprehensive overview, personal finance is, by definition, personal. Your unique situation — including your income, expenses, family structure, risk tolerance, and retirement timeline — will dictate the optimal strategy for your 2026 Retirement Contributions. If you feel overwhelmed or simply want a second opinion, consulting a qualified financial advisor can be invaluable.

A financial advisor can help you:

- Assess Your Current Situation: Get a clear picture of your finances.

- Define Retirement Goals: Help you articulate what a comfortable retirement looks like for you.

- Develop a Personalized Plan: Create a tailored strategy for your 2026 Retirement Contributions and beyond.

- Optimize Account Selection: Guide you in choosing the best accounts for your tax situation.

- Manage Investments: Assist with asset allocation, diversification, and rebalancing.

- Navigate Complex Tax Rules: Provide clarity on income limits, phase-outs, and strategies like the backdoor Roth.

- Stay on Track: Offer ongoing support and adjustments as your life circumstances change.

The cost of financial advice is often offset by the increased savings, tax efficiencies, and peace of mind you gain. Consider it an investment in your financial future, just like your 2026 Retirement Contributions.

Conclusion: Your Path to a Secure Retirement in 2026 and Beyond

Optimizing your 2026 Retirement Contributions is a powerful step towards building a robust financial foundation for your future. By understanding the various tax-advantaged accounts — 401(k)s, IRAs, Roth IRAs, and HSAs — and strategically maximizing your contributions, you can harness the power of compounding and tax benefits to accelerate your wealth accumulation.

Remember to prioritize employer matches, aim to max out your contributions across all eligible accounts, and consider your tax situation when choosing between pre-tax and after-tax savings vehicles. Stay informed about the official 2026 limits once they are released and adjust your plans accordingly. Furthermore, a sound investment strategy, regular rebalancing, and vigilance against common pitfalls will ensure your contributions are working as hard as possible for you.

The journey to a secure retirement is continuous. By taking proactive steps now to optimize your 2026 Retirement Contributions, you are not just saving money; you are investing in your future freedom, peace of mind, and the lifestyle you envision for your golden years. Start planning today, stay disciplined, and watch your retirement dreams become a reality.